After a decade of dormancy, in 2021 the Japan Atomic Energy Agency brought the High-Temperature Engineering Test Reactor (HTTR) project back online. HTGR has the potential to also add another color to the hydrogen rainbow. Hydrogen produced with nuclear power is labeled as pink. Japan NRG reached out to the JAEA for updates on HTTR development, funding and international cooperation.

Japan’s plans to build an offshore wind power sector largely rely on scaling up turbine size. Yet, it is the construction and installation technologies that will likely determine whether the sector succeeds. The logistics of assembling offshore wind power components can account for as much as half of total costs. Although Japan has exemplary logistics and transport networks for consumer retail, domestic firms have been slow to move into the offshore wind space; hence, European firms are taking the lead.

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Kyoko Fukuda (Japan) Magdalena Osumi (Japan Filippo Pedretti (Japan) Tim Young (Japan)

The Working Group of Experts for the Realization of GX, an advisory panel to the Cabinet, published an outline of the 2040 GX 2.0 strategy, which is an updated GX strategy PM Kishida announced in May.

It will have four focus points:

Energy – spurring investments into decarbonized power; expanding power transmission network; securing new power sources by exploring hydrogen and ammonia potentials; continuing to secure thermal power sources amid the transition;

Identifying GX industry locations such as supply bases;

Designing GX industry structure – introducing new processes to heavy emitting industries such as steel, speeding up commercialization of perovskite technologies, strengthening supply chains with allies;

Creating a GX market through effective carbon pricing.

The Working Group will meet in early August before the GX Implementation Council and will interview experts.

By the end of 2024, the Council will write a draft 2040 strategy.

CONTEXT: The GX Act was passed by Japan’s govt in July 2023, and it will drive ¥150 trillion worth of energy transition investments from the public and private sectors to realize carbon neutrality in 2050. However, officials say that the GX must simultaneously strengthen industrial competitiveness and achieve economic growth.

An ANRE experts panel working on the next Basic Energy Plan urged stronger state involvement in power supplies, as nuclear plants are aging and the increase in renewables capacity is slowing. If decarbonized power supplies don’t keep up with demand from the semiconductor and data center industries, then the growth of the national economy will slow, warned some panelists.

There were suggestions to increase support for small and medium-sized power operators and setting targets to spread installation of perovskite solar cell systems.

However, Takamura Yukari of Tokyo University warned that overestimating future demand will result in inefficient power which will raise power rates.

Murase Yoshifumi, the ANRE Commissioner, said the govt needs to set up a framework to improve visibility into power investments, adding that repurposing of thermal plants to generate decarbonized power is also important.

Senior members of the Liberal Democratic Party’s Mihama Town branch and Fukui Prefecture’s House of Councillors member Takinami Hirofumi met with METI’s Parliamentary Vice-Minister Yoshida Nobuhiro. They asked for replacement of current reactors with next-generation reactors in order to improve safety.

He also stressed the need for evacuation roads to Shiga Pref, and extension of the Hokuriku Shinkansen (bullet train) beyond Tsuruga.

Yamaguchi emphasized the town’s pride in being a “pioneer in hosting nuclear power plants”. Yet, there are challenges in maintaining a community that coexists with nuclear power and ensuring greater safety and security.

Yoshida explained that the GX Promotion Strategy approved by the Cabinet last year included plans to replace decommissioned reactors with next-gen reactors. He assured that METI would continue working towards this goal.

METI will study the international transfer of CO2 removal credits earned by Direct Air Capture (DAC), a technology that directly captures and stores CO2.

As a prerequisite for proceeding with an international agreement on the transfer of such removal credits, it’s necessary to consider which countries to prioritize, taking into account local legal regulations on CO2 capture and storage.

Promising countries include Australia and the U.S.

METI will consider efforts to coordinate the international transfer of CO2 removal credits based on the Paris Agreement.

TAKEAWAY: The majority of carbon credits relate to avoided emissions, through actions such as protecting the environment or replacing energy sources with cleaner alternatives. The act of removing CO2 from the atmosphere, however, is much more resource (and capital) intensive, and therefore results in more expensive carbon credits. Proponents of DAC and other CO2 removal technologies say that the removal credits should carry more weight or have some other differentiation factor to encourage their further development.

To expand demand for DAC credits, Japan needs to show progress on DAC and CO2 removal. The U.S. forecasts one billion tons of CO2 removal annually by 2050; the EU forecasts 400 million tons per year in 2040.

In December, JERA, JERA Cross and Shizen Connect, a VPP platform developer, will begin a trial for the supply of 24/7 carbon-free energy.

JERA and JERA Cross will act as aggregators of multiple power sources including renewables and batteries, and will forecast demand and power generation. Battery charging and discharging plans will be produced based on these forecasts.

Shizen Connect will control the batteries remotely, adjusting charging and discharging plans based on real-time monitoring of actual data to balance supply and demand.

Trial supply of 24/7 CFE for specific projects is expected to start in January 2025.

CONTEXT: There is growing interest in 24/7 CFE, which aligns hourly power consumption with supply to utilize renewables in real time; this is considered a more progressive approach than the current way of offsetting CO2 emissions through renewables certificates. JERA Cross has been researching 24/7 CFE tracking and certification with the University of Tokyo. To support this, JERA has invested in Shizen Connect.

ENECHANGE revised its consolidated financial results for 2023 in response to a review in the accounting of its EV charging subsidiary.

After the revision, the consolidated financial results announced in February saw sales decrease by ¥2.2 billion, while the net loss worsened by ¥3.7 billion.

To meet the criteria for a listing on the Tokyo Stock Exchange Growth Market, the company needs to improve its net assets to a positive value by the end of 2024.

CONTEXT: In February, ENECHANGE said it would raise about ¥4 billion through a third-party allotment of new shares, and expected net assets to be positive as of Q1 2024; but that forecast never materialized.

Amazon plans to increase procurement of renewables in Japan, sourcing from wind and solar farms to be built by Cosmo Energy and ENEOS subsidiaries by fall 2025. Amazon’s investment will be about ¥50 billion.

CONTEXT: A string of investments by tech giants such as Google should help accelerate the use of renewable energy in Japan.

Cosmo Eco Power, a subsidiary of oil refiner Cosmo, and ENEOS Renewable Energy, a subsidiary of ENEOS, inked a 20-year PPA. The firms will supply the power generated at their facilities directly to Amazon.

Amazon’s procurement of renewable energy in Japan is expected to increase by 60%. With the operation of the Cosmo and ENEOS power generation facilities, Amazon’s total annual power consumption in Japan is expected to increase to around 250 GWh.

Yamaha Motor will start a switch to hydrogen from city gas at its automotive component plants. Its remelter, which melts aluminum alloy ingots before they’re put into the casting machine for making wheels, etc, will be fueled by hydrogen to reduce carbon footprints.

In 2025, trial runs of a hydrogen-fueled remelter will begin at the Morimachi plant (Shizuoka Pref.). After over a year of tests, Yamaha’s other plants will also begin the transition, in 2027.

CONTEXT: Yamaha Motor uses an alloy called A356 that contains aluminum, magnesium and silicon, each with different melting points. Temperature controls are important to maintain quality consistency of final products such as vehicle wheels.

TAKEAWAY: In the aluminum production cycle, the metal is melted twice. First for making the alloy, by mixing aluminum and other elements, and secondly to process the alloy into wheels and other products. Energy efficiency improves if there’s only one melting process, but a solution hasn’t yet been found.

Itochu acquired a stake in ZeroAvia, a U.S. developer of hydrogen engines for aircrafts, and will represent the company in Asia.

The two also inked an MoU to collaborate on maintenance services, and to explore airport and hydrogen infrastructure opportunities in Asia.

CONTEXT: By 2032, ZeroAvia plans to develop hydrogen-powered, 200-passenger aircraft engines. It developed a 19-seat aircraft engine last year and has won pre-orders for 2,000 engines from airlines.

TAKEAWAY: ZeroAvia uses cryo-compression to store hydrogen, a technology combining liquefaction and compression methods. It competes with technologies developed by Japanese aircraft engine makers. Cryo-compression and liquid hydrogen face similar challenges: to keep the storage container completely insulated, to make it smaller and reduce the weight.

Starting 2026, Yokohama-based Automotive Energy Supply Corporation (AESC) plans production in Spain of lithium iron phosphate (LFP) batteries for EV and energy storage systems.

This will be one of Europe’s first mass LFP production. AESC has invested over a billion euros for the first phase of LFP production.

CONTEXT: LFP does not use nickel or cobalt, and has been a cheaper alternative to lithium ion batteries. It has spurred the EV market expansion in China.

TAKEAWAY: Nikkei reported that AESC is studying LFP production in Japan. Some industry observers have blamed high battery costs, as well as limited charging stations, as the cause of Japan’s slow transition to EVs from gasoline vehicles. Lithium prices are dropping in recent months due to weaker demand in China. In theory, the lower prices should boost sales of not just LFP but also more expensive lithium ion batteries.

ClassNK and Singapore to step up methanol, biofuel bunkering guidelines

(Japan NRG, July 9)

ClassNK plans to step up efforts to write methanol bunkering guidelines, working with Singapore’s Ministry of Transport and local bunkering service providers.

On July 2, ClassNK and Singapore-based Yanmar Asia, Taiko Asia Pacific and Consort Bunkers signed a MoU to explore vessel equipment details required for methanol and biofuel bunkering.

The framework will be crucial in updating Japan’s bunkering guidelines, ClassNK told Japan NRG.

CONTEXT: The Ministry of Land, Infrastructure, Transport and Tourism will write the bunkering guidelines with input from Japan Coast Guard and the shipping sector. The guidelines cover marine fuel oil and LNG; studies on ammonia bunkering began in January. Methanol and biofuel have not yet entered the study scope.

TAKEAWAY: Singapore has the world’s largest bunkering operations. In December 2023, Japan and Singapore launched the Green and Digital Shipping Corridor to develop standards for new shipping fuels. As a result, Japan would be importing methanol and biofuel standards, while likely exporting ammonia standards once developed.

ORIX ordered two dual-fuel bulk ships from Tsuneishi Shipbuilding that use methanol and marine fuel oil; and another dual-fuel bulk ship was ordered from Oshima Shipbuilding.

CONTEXT: This is ORIX’s first order for methanol-fueled ships. This December, Mitsui OSK Lines will sail Japan’s first methanol-fueled ship for inland transport.

NYK agreed to take an 80% stake in a new company that will take over ENEOS Ocean’s non-crude oil tanker businesses. It includes LPG ships, chemical tankers, product tankers, and cargo ships.

The new company will operate 49 ships in total — 18 LPG ships; 19 chemical/product tankers; and 12 cargo ships. It will include 16 subsidiaries, including operation and ship management companies in Singapore.

Oshima Shipbuilding delivered a bulk carrier Wind Challenger, which is mounted with a propulsion system powered by wind, to Mitsui OSK Lines. MOL Drybulk will operate the ship.

Emissions are cut by 7-16% depending on the ship route and other conditions.

CONTEXT: MOL plans to own nine Wind Challenger vessels, and this is the second. The future Wind Challengers will have electrolyzers on-board to produce green hydrogen while sailing. MOL’s ultimate goal is zero-emission sailing.

METI is soliciting public feedback on its plan to change the criteria of Japan Investment Corp decisions. Submissions are due Aug 16.

The new criteria will clarify that the green transformation and digital transformation are essential for strengthening the competitive strength of Japanese businesses. The present criteria do not address GX or DX directly.

CONTEXT: JIC is a public-private financing vehicle mostly funded by the govt, and with a minor contribution from 24 companies that includes ENEOS and Osaka Gas.

METI Minister Saito, Foreign Minister Kamikawa, and 10 ministerial-level delegates from the League of Arab States joined the 5th Japan-Arab Economic Forum in Tokyo.

They shared views on sustainable and resilient economic development, energy and economic security cooperation, resources development, etc.

Hokkaido University set up the Renewable Energy Research & Education Center (REREC) for renewables tech and Human Resources in tech.

The center will work with local universities and vocational schools.

CONTEXT: Hokkaido has high potential for renewables due to its climate and geography. The region, however, also faces population decline — falling birthrates, and an aging population — which are reasons for the govt’s push towards sustainable urban development.

GE Vernova, a U.S. energy equipment manufacturer, says that Japan’s curtailment rate could reach 25% of operating renewables capacity by 2030 due to the growth of renewable energy and the restart of nuclear power plants.

CONTEXT: Curtailment results in a lower efficiency of assets since they are forced to operate below potential capacity.

The U.S. firm looked into four scenarios, based on the planned restart of NPPs and expansion of renewables.

If more NPPs restart than planned, and renewable energy continues expanding smoothly, then the curtailment rate for renewable energy is forecasted to be 25%.

CONTEXT: At present, Kyushu is the region with the highest level of curtailments in Japan, a rate that hit 8.3% of capacity in FY2023.

By 2050, curtailment rates could even be higher – above 30%, if the number of nuclear units online are more than planned.

GE Vernova believes that electricity supply could be stabilized by introducing more gas-fired power generation and hydrogen production tech.

TAKEAWAY: Grid connectivity is seen as one of the biggest challenges faced by local utilities in stabilizing the power grid. GE Vernova’s forecast appears to be based on the current trend, echoing growing concerns in Japan that the curtailment rate will only increase. However, with investments in grid connectivity and BESS tech to address grid congestion, the curtailment rate could be reduced.

Inpex plans to invest more than ¥200 billion yen ($1.25 billion) in Australian renewables projects through 2030. This includes creating power sources to create ‘green’ hydrogen for export to Japan.

Itochu’s JV with Italian utility Enel, Enel Green Power Australia, will boost its renewables capacity from about 300 MW to between 2 GW and 4 GW at the end of the decade. The additions should be mostly split between solar, onshore wind and storage batteries.

Some of the electricity from the new projects will be used to power the Ichthys LNG project, operated by Inpex, after 2030.

For storage batteries, Inpex plans to utilize the supply and demand adjustment market and also pursue retail sales.

Further along, Inpex will explore green-hydrogen manufacturing options in Australia.

NRA Chairman Yamanaka Shinsuke visited TEPCO’s Fukushima Daiichi NPP to inspect the facilities related to the retrieval of melted nuclear fuel debris.

The planned retrieval is scheduled to start as early as August.

Yamanaka checked entry ways for bringing in robotic arms to retrieve the debris, as well as the sealed containers.

TAKEAWAY: Starting debris removal is essential for evaluating its composition. Also, it’s important to improve decommissioning and reduce ongoing contamination. As TEPCO can only remove debris in small quantities at a time, it might take decades. What’s more, there are many uncertainties over where to store and how to manage contaminated waste.

TEPCO will set up a new department to develop plans for and manage the decommissioning of the Fukushima Daiichi NPP. The new department will be called the “Decommissioning Strategy Office,” and will start on August 1.

It plans to start trial retrieval of fuel debris by the end of FY2024.

Two cases of unauthorized access were recorded at the Kashiwazaki-Kariwa NPP in March. Two workers brought smartphones into a restricted area with no permission.

The workers forgot about the smartphones, and security guards did not notice.

The incident raises concerns over security at the plant.

CONTEXT: TEPCO owns and operates Kashiwazaki-Kariwa NPP, which was once the largest NPP in the world by capacity; Unit 7 is penciled in for a restart in October. However, the plant operator is still trying to convince the local authorities to give it the final go-ahead.

Fukui Pref and Takahama Town gave KEPCO approval for an operation extension of Takahama NPP Units 3-4.

KEPCO reaffirmed its commitment to the safety of its NPPs.

CONTEXT: Operational since November 1974, Takahama’s four units have a total power capacity of 3.4 GW. Since the upgrade of the safety standards in the aftermath of the Fukushima disaster, nuclear operators have additional checks every 10 years on facilities that are 30 years old and above.

TAKEAWAY: The process of extending NPP operations is smoother compared to restarting reactors. While the latter involves consent of the local community, a condition that’s not required by law but essential in practice, extending operation does not.

KEPCO secured approval from Fukui Pref and Takahama Town to proceed with changes in Takahama NPP Units 1 and 2 relating to a reactor installation permit for replacement of in-core structures.

On July 8, TEPCO Power Grid received electricity from Chubu Electric Power Grid due to higher-than-expected temperatures that boosted demand amid increased air conditioning use.

Up to 200 MW of power was sent between 9 a.m. and noon, as the reserve ratio in TEPCO’s service area fell below the 3% buffer required for reliable supply.

The firm said it recorded peak demand after 2 p.m., at 54.9 GW.

This is the first time in about two years, since August 2022, that TEPCO has had to receive power from another company.

KEPCO subsidiary Kansai Transmission and Distribution also received electricity from Chubu Electric PG due to extreme heat. The firm’s reserve ratio temporarily fell below 3% after 6:00 p.m. It received 360 MW from 6:30 p.m.

The Tokyo area had severe heat on July 9, with max electricity demand exceeding 50 GW for the second day in a row. However, power transfer was not required.

CONTEXT: So far this year, the number of power transfer cases is already the third highest after 24 incidents nationwide in 2022 and 17 in 2018.

TAKEAWAY: The heat wave in Japan has energy firms looking for more LNG cargoes to meet increased demand as the heat boosts A/C use and power demand.

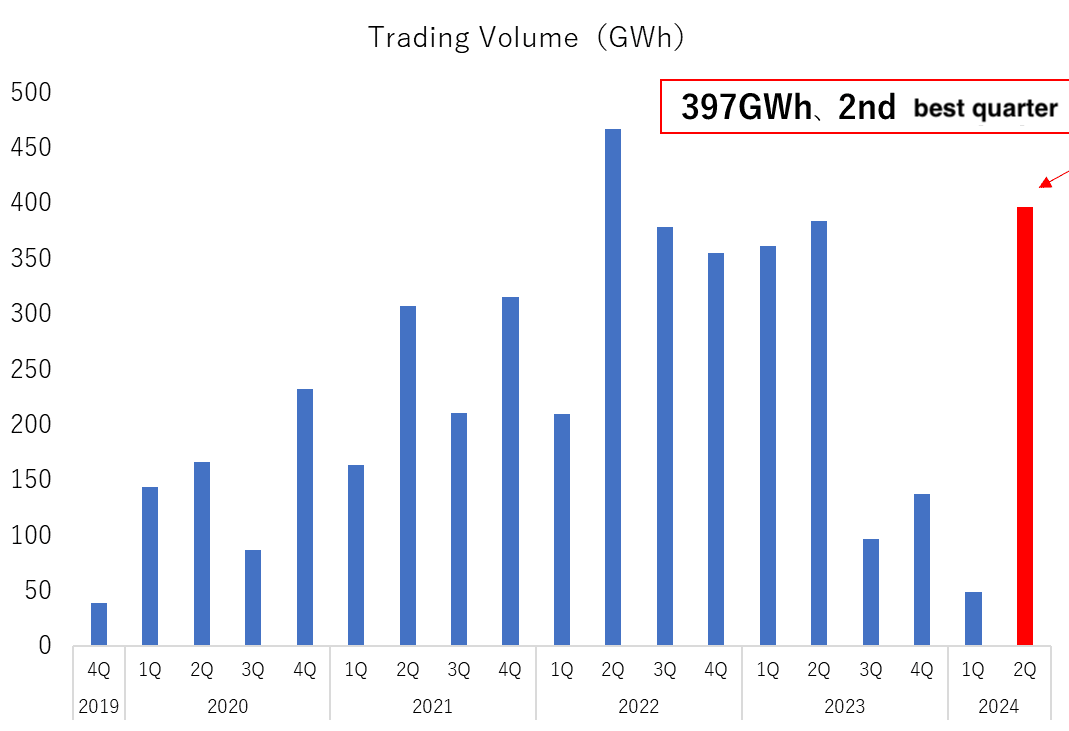

TOCOM power futures have second-best quarter on record

(Exchange statement, July 11)

Trading volume for the second three-month period of 2024 reached 397 GWh, the second-highest for a quarterly period since the contract was launched in 2019. TOCOM attributed the rising volumes partly due to the introduction of the market maker system in April.

Sumitomo will use the capacity market to trade and secure electricity supply for an energy storage system in Chitose City, Hokkaido.

The company aims to use OCCTO’s capacity and supply-demand adjustment market (balancing market) to improve profitability.

Sumitomo has participated in capacity market auctions for three years in a row since FY2021, and is set to provide power capacity for the grid in Chitose starting FY2025, sourcing power from storage batteries.

This is Sumitomo’s first commercial use of grid storage batteries. It’s powered by batteries from Nissan Motor’s EV LEAF, the largest of its kind in Hokkaido.

Osaka Gas, Mizuho Lease Power, JFE Engineering and Kyushu Steel will develop an energy storage system, Takeo Grid Storage, in Takeo City, Saga Pref.

The firms aim to start commercial operation by late 2025, and plan to use lithium-ion batteries with a 8 MWh capacity and 2 MW output.

Osaka Gas will manage operation of storage batteries and trading on electricity markets (wholesale, balancing and capacity markets).

This will be Osaka Gas’ second investment in the grid storage battery business, following Senri Grid Storage.

CONTEXT: Saga Pref is in the northwest of Kyushu, located in south Japan. The Kyushu region is Japan’s leading supply of solar power and oversupply often leads to power curtailments, requiring grid stabilization. Grid congestion is a major reason for power curtailment. In Kyushu, the curtailment rate soared in FY2023, reaching up to 7-8% of renewables capacity.

Aomori Pref and Mutsu City met to discuss plans for an interim storage facility for spent nuclear fuel. Mutsu City residents raised concerns about the final destination of the spent fuel after 50 years.

Representatives from Recyclable Fuel Storage (RFS), TEPCO, Japan Nuclear Fuel, and govt officials attended.

A key focus was Article 4 of the safety agreement, which stipulates a 50-year storage period for the spent nuclear fuel before its transportation to a reprocessing plant. The interim storage facility, in theory, manages the fuel until it can be reprocessed.

RFS aims to begin operations of the first storage building by September, with plans for a second building.

CONTEXT: RFS is a company founded by TEPCO and Japan Atomic Power Co. It’s dedicated to building the facility in Mutsu.

TAKEAWAY: As in the case of KEPCO’s fuel temporarily stored on the NPPs’ premises, local consent relies on the promise of future transportation to long-term and reprocessing storage facilities. However, the considered final destination – the Rokkasho spent nuclear fuel reprocessing plant – has faced delays for 31 years, as the NRA requests safety improvements. Until the govt can offer a concrete long-term solution for spent nuclear fuel, the short-term and mid-term storage facility projects will be met with skepticism by locals.

Hokkaido became the only area to have met the target level of supply reliability in OCCTO’s additional capacity market auction for FY2024 (delivery in FY2025).

The auction was offered only in three regions, with a total capacity of 1.33 GW — Hokkaido (584 MW), Tokyo (295 MW), and Kyushu (453 MW).

The contract price was ¥13,761/ kW in Hokkaido; ¥3,495/ kW in Tokyo.

CONTEXT: To date, the nationwide supply capacity secured for FY2025 is 184 GW. Since Hokkaido, Tokyo, and Kyushu exceeded their annual outage limit, and supply reliability was insufficient, an additional auction was held in these three areas.

OCCTO said that as of late June the number of consumers nationwide switching retail electricity providers rose 327,200, from the end of the previous month to a total of 3,052,000.

By the end of June, compared to May, the switching rate increased by area the most in Kansai, Tokyo, and Hokkaido, and the least in Hokuriku, Okinawa, and Tohoku.

Pacifico Energy inked a loan with Mitsubishi HC Capital and its subsidiary, BOT Lease, to finance a solar PV project (134 MW capacity) in Tsu City (Mie Pref).

The installation will take 26 months, and is set to launch in 2026. Commercial operation is set for 2028.

CONTEXT: Pacifico Energy has developed 15 solar farms nationwide under the FIT; the project in Tsu is the second developed for the corporate PPA under the FIP.

A group of firms led by the New Energy and Industrial Technology Development Organization has launched Japan’s first wind observation and test site in the port of Mutsu-Ogawara, Rokkasho (Aomori Pref).

The initiative seeks accuracy of remote sensing equipment used for wind observation.

CONTEXT: Commissioned by NEDO, other partners include Kobe University, as well as several startups at the university; the Japan Weather Association; offshore engineering firm Kitanihon Kaiji Kogyo, etc.

Through its wholly owned subsidiary MBK Investment Management Netherlands, Mitsui & Co made a final investment decision on the Ruwais LNG project that’s in partnership with Abu Dhabi National Oil Company (ADNOC) and other investors.

Located in Abu Dhabi, this midstream natural gas liquefaction project will have an annual production capacity of 9.6 million tons; it is set to begin production in 2028.

The development costs primarily consist of the EPC cost for the LNG plant. The contract value of the EPC is about $5.5 billion, which would equate to $550 million for Mitsui in line with its equity share.

CONTEXT: This represents Mitsui’s return to the Middle Eastern LNG market where the company first ventured in the 1970s. Mitsui has been cooperating with ADNOC for around 50 years.

The Japan Bank for International Cooperation inked loan agreements with Mitsui Oil Exploration Co.

JBIC also signed the agreements with MOECO Vietnam Petroleum, and MOECO Southwest Vietnam Pipeline.

The loan total for all JBIC partners is nearly $1.25 billion.

The funds will help develop the Block B gas field off the southwest coast of Vietnam, as well as pipeline construction for supplying fuel gas to thermal power plants.

CONTEXT: Vietnam aims to achieve carbon neutrality by 2050. The country will reduce coal use, and increase gas and LNG for power generation.

Japan faces an aviation fuel shortage due to oil refinery shutdowns and new regulations limiting truck driver overtime.

The shortage has already affected several airports — Narita, Hiroshima, and Fukuoka. Most impacted by delays are new international routes and charter flights.

MLIT plans to add three tankers to domestic routes. Japan will also import fuel from South Korea and increase fuel transportation via tanker trucks.

The govt will set up a data collection system from airports to inform fuel suppliers about new routes and charter flights.

CONTEXT: Japanese refineries produced 1,157,052 kiloliters (7.3 mln barrels) of jet fuel in May, up 18.7% YoY, and imported 5,876 kl, flat YoY. Domestic sales, including domestic and imported jet fuel, were 368,649 kl, up 9% YoY. During the month, Japan exported 708,293 kl, up 0.4% YoY.

TAKEAWAY: According to ANRE, the end-May jet fuel stocks stood at 826,515 kl, up 5.2% YoY and up 10.4% MoM. The shortage appears to be in limited areas due to a lack of domestic transport means, or the govt would have asked the refineries to suspend exports. The introduction of strict overtime limits on truck drivers in Japan from April 2024 has affected a number of industries because there’s a general shortage of drivers in the country. Record inbound tourism numbers have added to the demand picture.

LNG stocks of 10 power utilities were 1.98 million tons as of July 7, down 5.7% from the previous week (adjusted to 2.1 million tons). This is 2.1% up from a year ago (1.94 million tons), and 9.6% down from the past 5-year average of 2.19 million tons for the end of July.

CONTEXT: There’s been a surge in use of gas-fired power plants to meet additional power demand due to heat. Output from the gas plants in the Tokyo region is up by close to half on the previous month.

CONTEXT: The Japan Weather Association predicts that the rainy season will end in the third week of July in south Japan, and a week after for the northern part. Except for the Tohoku area, the rainy season is due to last a bit longer than usual.

ANALYSIS

BY FILIPPO PEDRETTI

Hydrogen’s Atomic Dreams: Japan Aims for Hydrogen Production With Nuclear Power

In early 2010, a High-Temperature Engineering Test Reactor (HTTR) in the town of Oarai, northeast of Tokyo, generated a temperature of 950°C that was enough to help produce hydrogen for 150 hours. The Japan Atomic Energy Agency (JAEA) and others thought that a cost and energy efficient way of producing hydrogen had been found.

Those hopes were dashed in March 2011 when the Fukushima Daiichi disaster led to a shutdown of the country’s entire nuclear power fleet.

After a decade of dormancy, in 2021 the JAEA brought the HTTR project back online, as well as the research. A new milestone was reached in March this year when a safety demonstration test proved that the reactor could cool by itself in case of an accident. This has reignited hopes for nuclear power-based hydrogen production.

High-temperature, gas-cooled reactors like the HTTR have the potential to also add another color to the hydrogen rainbow. While colors like green, blue and gray have been popular in describing, respectively, hydrogen production via renewables, CCS, and fossil fuels, hydrogen produced with nuclear power is labeled as pink.

International competition is one reason why Japan has restarted its program. Poland, the UK and the U.S. all have similar projects. China, however, has made the most progress, launching in December 2023 the world’s first modular high-temperature, gas-cooled reactor nuclear power plant; this HTR-PM features two small reactors (each 250 MW) that uses helium as coolant and graphite as the moderator.

Japan NRG reached out to the JAEA for updates on the HTTR development, funding and international cooperation.

The test, the reactor

On March 27-28, the JAEA did a safety demonstration test for the 30 MW HTTR reactor. Among the five next-generation advanced reactor types designated by the government in the latest nuclear industry roadmap, the high-temperature gas-cooled reactor (HTGR) is expected to be one of the first to reach the proof-of-concept test stage. The HTTR design is the first example of an HTGR in Japan, and the JAEA seeks to advance it to make a commercial system.

The JAEA conducted the test at 100% power at the Oarai Research & Development Institute (Ibaraki Prefecture) without inserting control rods and with the coolant flow set to zero. They stopped the helium circulator, thus losing the forced cooling function. It confirmed that the reactor could decrease its output, cool down and stabilize by itself.

The reactor’s enhanced safety features is a key advantage, together with the possibility of hydrogen manufacturing. In theory, the reactor won’t suffer a core meltdown in case of an accident.

The reactor’s key component is the graphite in the core that can endure high temperatures. Unlike most reactors (which use water), the HTTR uses helium gas for cooling. The core has a large heat capacity, and the test showed that even during an incident the temperature changes gradually due to the graphite, which can withstand heat up to 2,500°C.

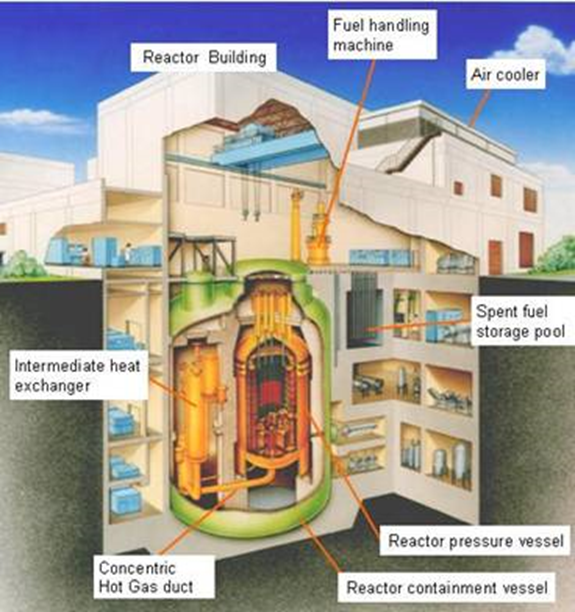

The HTTR facility

Source: JAEA

Schedules and funding

The government has a schedule for developing a demonstration high-temperature gas-cooled reactor. According to the “Basic Policy for Realizing GX” the start of operations is expected in the 2030s. METI’s Innovation Reactor Working Group also established a roadmap for the construction of the demo reactor.

ANRE began the HTGR Demonstration Reactor Development Project in FY2023. Through public recruitment, they selected Mitsubishi Heavy Industries (MHI), which handles basic design and future manufacturing of the HTGR Demonstration Reactor. Following this, MHI began the basic design of the demo reactor in the same year.

As for funding, in FY2023, the government allocated ¥1.83 billion for R&D of HTGR and its heat use technology. In FY2024, funding was ¥2.27 billion. Also, under the GX Promotion Measures, ¥4.8 billion was given in FY2023 for the “HTGR Demonstration Reactor Development Project”. Another ¥127.9 (¥43.1 billion + ¥84.8 billion) has been allocated for the budget from FY2023 to FY2027. JAEA said that, together with MHI, it will proceed with development based on the technical roadmap for the introduction of HTGR.

Hydrogen production

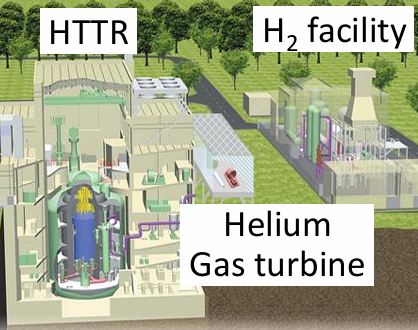

JAEA said there are plans for R&D using the HTTR, but it’s considering connecting a hydrogen production facility to it. This will be the first such unit in the world and should prove that hydrogen can be made using heat from a reactor.

Source: JAEA

Japan has considered producing hydrogen via nuclear power for a while. The electrolysis process that splits water into hydrogen and oxygen can be powered with electricity from solar or wind farms. Yet, due to their low operational rates, the amount of time that the electrolysis equipment is operating drops, leading to higher costs. The other mainstream way of making hydrogen utilizes fossil fuels.

Turning to a nuclear facility like the HTTR may provide a hydrogen manufacturing option that doesn’t rely on hydrocarbons or the vagaries of the weather. Its proponents also say it will be a cheaper alternative to ‘green’ hydrogen made with electricity from renewables.

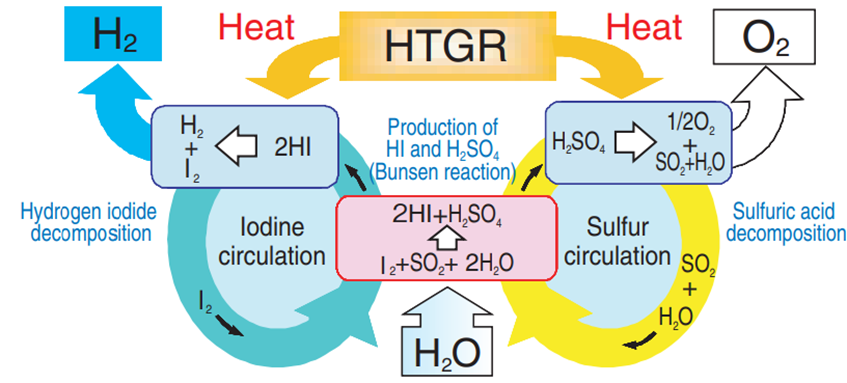

The government plans to use HTTR’s heat for producing hydrogen via the Iodine-Sulfur (IS) process that involves thermochemical water splitting using high-temperature heat sources. It combines iodine and sulfur chemical reactions. In the process, the temperature for water decomposition is lowered from about 4,000°C to below 900°C.

The iodine and sulfur are recycled, resulting in the decomposition of water into hydrogen and oxygen. To prove the commercial viability of this approach, HTTR tech will need to scale up the reactor’s thermal output, from 30 MW to around 600 MW.

IS Process. Source: JAEA

International cooperation

The JAEA is also keen on international collaboration with countries pursuing HTGR projects. Currently, collaborations are progressing with the UK and Poland. The UK government selected HTGR as an innovative reactor for the non-power sector towards net-zero GHG emissions, and began the HTGR Demonstration Reactor Program in September 2022. This program has three phases:

Phase

Content

Date

Phase A

Preliminary concept review

Completed February 2023

Phase B

Basic design

Scheduled to complete by March 2025

Phase C

Licensing, construction, and operation

Start in the early 2030s

In July 2023, the Department for Energy Security and Net Zero (DESNZ) selected a team for Phase B’s contractors, comprising the UK National Nuclear Laboratory (NNL) and the JAEA as one of them. NNL and JAEA will conduct the basic design of an efficient heat-utilizing UK HTGR Demonstration Reactor, including hydrogen production or steam use.

During Phase B, DESNZ announced the start of a fuel development program for the HTGR Demonstration Reactor. It selected NNL as the contractor in July 2023. JAEA, along with Nuclear Fuel Industries, will collaborate with NNL. The goal is to establish commercial-scale fuel manufacturing technology in the UK, and will be based on Japan’s HTGR fuel design and manufacturing technology. Technology transfer will involve concluding technology and license agreements, making UK-produced HTGR fuel one of the procurement options for domestic HTGR demo reactors.

Poland plans to use HTGR as a heat source for the chemical industry. It will thus replace coal-fired power to achieve decarbonization and aims to introduce an HTGR research reactor (thermal output of 30 MW) in the late 2020s. The National Center for Nuclear Research (NCBJ) is in charge of advancing the HTGR research reactor design. In September 2019, the JAEA signed a R&D agreement with the NCBJ.

Conclusion

Many of Japan’s industrial titans want the country to seize this opportunity in nuclear power. A recent Nikkei survey of 100 Japanese executives showed how the majority was in favor of restarting existing NPPs and building new ones. On the other hand, a feeling of skepticism towards nuclear power persists among Japan’s population. The government, however, is adamant in restarting nuclear power plants and having nuclear power account for up to 22% of the national energy mix by 2030. While the deadline is near, many plants are still idling.

Progressing with HTGR technology may bring a breath of fresh air to the nuclear sector. Given its smaller size and boosting enhanced safety, as well as its potential for producing hydrogen, HTGR may encounter less resistance compared to traditional reactors.

HTGR, together with other new advanced reactor types and technologies such as fusion and SMRs, may take a role in reshaping the future nuclear industry. The possibility of producing hydrogen may also open a different possibility for nuclear energy than the hardline, straightforward NPPs restart approach.

This can happen only if the HTGR reaches a commercialization phase, which still seems very distant. What’s more, it must prove its commercial viability. To beat the competition with the CO2 hydrogen production method, it cannot rely on its own forces alone, but it needs the help of state measures such as carbon pricing and carbon tax.

ANALYSIS

BY MAGDALENA OSUMI

Solving Logistics Barriers: Transport Solutions for Wind Farm Components

Japan’s ambitious plans to build a sizable and competitive offshore wind power sector largely rely on scaling up turbines in local projects. Yet, it is the construction and installation technologies that will likely determine whether the sector succeeds, and which companies race ahead.

The logistics of assembling wind power generation components, moving them to the location of the wind farm, and then assembling facilities, can account for as much as half of total offshore wind project costs. In Japan, the numbers tend to be at the higher end of the range due to a dearth of domestic component transportation options on land and sea, as well as lagging port infrastructure. As a result, many local developers are scrambling to find ways to cut both capital, operating and future decommissioning expenses.

Japan’s obvious need to accelerate wind sector supply chain development has created opportunities for a number of European firms with tech solutions tested in their regional markets. Although Japan has exemplary logistics and transport networks for consumer retail, domestic firms have been slow to move into the offshore wind space.

By the early 2030s, Japan seeks to operate 10 GW of offshore wind capacity. For onshore wind, expectations are even higher – as much as 26 GW installed nationwide. Many of these projects are still on the design board or in early stages of development, with delivery of electricity scheduled from 2028 on out. But in terms of project management, this means solutions are needed today.

Installation woes

Industrial wind turbines are massive pieces of high-tech that require sophisticated equipment to transport them from manufacturing facilities to hubs or ports for final assembly, and then from there they’re delivered to final designated sites. The typical three-blade wind turbine consists of a tower, nacelle, rotor, and three blades spanning up to 100 meters.

Japan’s most widely used turbines are made by General Electric, and Siemens Gamesa Renewable Energy. Vestas’ 4.2 MW turbine is also used in large-scale projects; it has a tower ranging between 105 and 166 meters high, blades spanning 76 meters, and nacelles measuring almost 13 meters. Each blade can weigh up to 70 metric tons. Needless to say, moving these parts is a challenge.

Technological innovations in wind power generation are proving to be a double-edged sword. While increasing wind turbine component size helps to boost capacity, it also negatively impacts the lifting, loading and transport of components. In addition, Japan’s specific topography with mountainous terrain and narrow roads, as well as local transport regulations, further compounds logistical challenges.

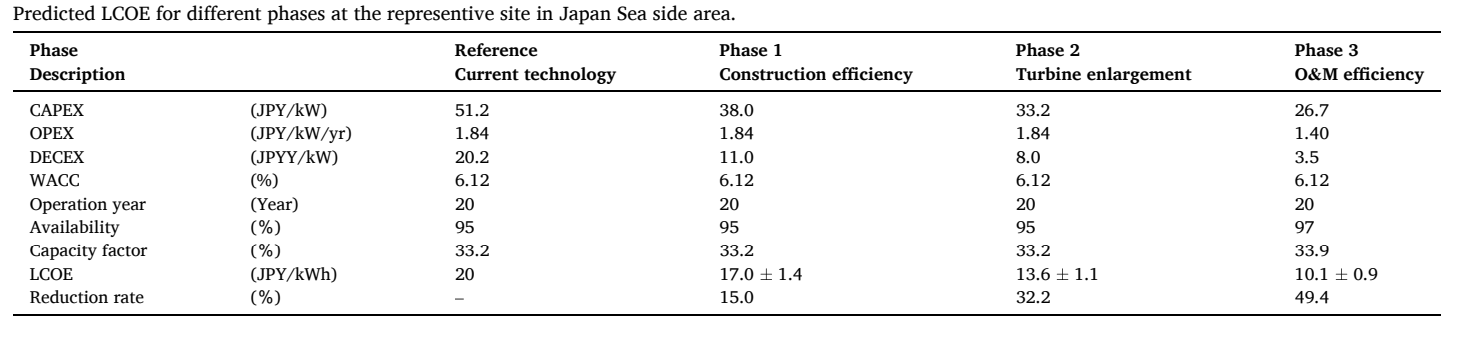

In fact, increasing turbine size will play only a partial role in Japan’s efforts to reduce the cost of electricity produced by offshore wind farms, according to a 2023 study by academics Kikuchi Yuka and Ishihara Takeshi at the University of Tokyo’s School of Engineering.

In an article published in Applied Energy 341 (2023), the two academics used data from some of Japan’s tops engineering firms and reviewed the development of the UK’s offshore wind sector to conclude that domestic projects will need to rely as much on efficiencies from the construction and operations and management (O&M) phases as on bigger turbines to help meet the government’s levelized cost of electricity goals for the sector.

Source: Applied Energy 341 (2023), Y. Kikuchi and T. Ishihara

Moving to bigger turbines also brings its own challenges. As wind farm operators move towards using turbines with a capacity of up to 15 MW or more, standard transporters are often too small or are not suitable to carry heavy components measuring several dozen meters in length. Even for a typical 1.5 MW turbine, you can expect a blade length between 35 and 45 meters. While such a size is manageable for transport, larger units require more specialized trucks.

To address this, construction companies and developers in Japan are looking to markets with more advanced wind power sectors for inspiration. They’re adopting innovative solutions, such as blade transporters offered by Belgian firm Faymonville, whose lifters can transport blades either horizontally and vertically. This is useful in hilly areas. The lifter rotates on its own axis and can swivel to the side.

In 2016, Faymonville entered the Japanese market, and now offers a range of loaders, flatbed trailers, modular and other types of 6-axle, 4-axle and 2-axle trailers and semi-trailers for special or heavy transport. Clients include Nippon Express, Japan’s leading firm in the transport sector.

Faymonville also offers low-bed trailers to transport other components like nacelles or towers. The vehicles have floors that can widen or lower in accordance to the component height and size when passing through tunnels or under bridges, or through other narrow and uneven areas.

The Belgian firm says that Japan tops the list of countries conducting tests using its latest trailers for wind projects. This year, the seventh of its bladelifter trailers was set to be delivered to Japan.

Trailers with flexible blade lifters also enable project operators to avoid additional pricing levied by law for the use of properties adjacent to the road in case the transported cargo even slightly crosses over such an area, as well as the cost of chopping down trees to make way for the trucks to sites in remote areas.

Problems at the sites

Advanced tech solutions for moving components, however, won’t address potential problems at sites where turbines are assembled or from where they are, for instance, transported offshore. Challenges in port logistics range from the lack of space for assembly to approval of such work by local fisheries and other special interest groups.

Many of those sites often have poor infrastructure unable to accommodate the large-scale equipment used to assemble massive components, never mind the components themselves. The problem is also due to the scarcity of land and regulatory constraints in port areas. (In a separate article, Japan NRG will focus on the challenges at port areas and their use for wind power generation projects.)

Another innovative solution comes from Heavy Duty Pavements, a Dutch consulting firm, which offers “soil stabilization solutions” – upgrades of ground bearing capacity at project sites. This enables project operators to quickly strengthen the ground for assembly or transportation of components.

While not yet available in Japan, the firm’s solution enhances the load bearing capacity of the soil up to required ground bearing pressure. During a recent energy trade show in Tokyo, the firm demonstrated its so-called Enviro-Mat additive, which enhances cement by lengthening its crystals, creating a more durable bond.

The company claims that its technology increases safety and is cost efficient as the reinforced layer can be quickly installed and removed. It also makes the ground resistant to water and freeze-thaw damage, making it suitable even for harsh climate conditions.

This is important because several offshore wind farm sites are near Hokkaido, which is surrounded by the Sea of Okhotsk, the Sea of Japan and the Pacific Ocean. In winter, these areas can face heavy snows with temperatures below freezing.

With more than 10 offshore, onshore and near-onshore wind power projects in the pipeline, Japan is faced with an opportunity to invest in more advanced technologies to address logistical challenges in the wind power industry. Their innovative solutions will become crucial with further advancement of wind turbine technology in Japan.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific

Australia / Data centers

Due to the growth of AI, the country needs 3.3 to 5 GW of additional capacity by 2030, or about 15% of the current total load, according to UBS. Data centers now account for almost 25% of large industrial power demand in Australia. UBS forecasts that load will increase by 16% annually through 2030.

China / Vehicles

The number of motor vehicles reached 440 million, including 345 million cars and 24.72 million new energy vehicles.

China / Power grid

Through 2030, the electricity grid will invest more than $800 billion to upgrade. The aging grid is a major constraint for China’s energy transition. During the first four months of 2024, China invested $17 billion in power grid projects, a 25% YoY increase.

China / Solar power

The Industry Ministry issued rules tightening investment regulations for solar PV projects. They’ll need to have a minimum capital ratio of 30% with the new rules. Previously, the minimum for PV projects was 20%.

India / Coking coal

This month, India will import coking coal from Mongolia on a trial basis. India seeks to diversify imports of the steelmaking raw material to mitigate over-reliance on Australia.

India / Hydropower

India plans to spend $1 billion to expedite the construction of 12 hydropower stations in the Himalayan state of Arunachal Pradesh. This could raise tensions with China that also lays claims to the region.

India / Pumped storage

The country’s pumped storage capacity is expected to reach about 55 GW by 2031, up from the current 4.7 GW, said the Ministry of Power. India has around 2.5 GW of pumped storage capacity under construction. Around 50 GW of other similar projects are under different stages of development.

Pakistan / Power prices

Amid rising power prices, consumption of electricity from the national grid fell 10% in FY2023. This exacerbates problems in the crisis-ridden electricity sector, which is straining under $8.3 billion of debt, much of it owed to Chinese energy producers.

Southeast Asia / Natural gas

Offshore gas production in the region has a $100 billion potential, driven by many FIDs expected to materialize by 2028, says Rystad Energy. This is a more than twofold increase over the $45 billion in developments that reached FID from 2014 to 2023.

Vietnam / Solar power

A new rule could unleash a surge in solar and wind energy, where companies from Apple to H&M hope to switch their supply chains to renewable power. Under the so-called Decree 80 issued last week, Vietnam now allows businesses to buy renewable energy from producers instead of relying on state monopoly Vietnam Electricity.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

January

First market trading day (Jan 4)

IEA “Renewables 2023: Analysis and Market Forecast to 2028” released (Jan 11)

Renewable Energy Exhibition (Jan 31 – Feb 2)

Taiwan presidential election (Jan 13)

Japan’s Diet convenes

IEA “Electricity 2024 / Analysis and Forecast to 2026” released (Jan 24)

February

CFAA International Symposium (Feb 2)

India Energy Week 2024 (Feb 6-9)

Lunar New Year (Feb 10-17)

Indonesia presidential election (Feb 14)

Japan-Ukraine Conference for Promotion of Economic Reconstruction (Feb 19)

FIT/FIP solar auction (Feb 19 – March 1)

Smart Energy Week (Feb 28-Mar 1)

March

Announcement of auction result for Offshore Wind Round 2 (for Akita Happo-Noshiro Project)

Onshore wind auctions (March 4-15; results on March 22)

International LNG Congress (LNGCON) 2024, Milan, Italy (March 11-12)

Russian president election (March 15-17)

World Petrochemical Conference, Houston, TX, USA (March 18-22)

IAEA Nuclear Energy Summit @ Belgium (March 21)

Ukraine presidential election (due before March 31)

Happo Noshiro, Murakami-Tainai, Oga-Katagami-Akita and Saikai-Eshima wind project auctions close (June 30)

July

Tokyo governor election (July 7)

7th Basic (Strategic) Energy Plan draft published (expected)

August

7th Basic (Strategic) Energy Plan draft presented to Cabinet (expected)

September

Global Offshore Wind Summit Japan 2024, Sapporo, Hokkaido (Sept 3-4)

The United Nations Summit of the Future (Sept 22-23)

Gastech 2024, Houston, TX (Sept 17-20)

IAEA General Conference

GX Week in Tokyo (expected late Sept to October)

Asia Green Growth Partnership Ministerial Meeting

Asia CCUS Network Forum

International Conference on Carbon Recycling

International Conference on Fuel Ammonia

GGX x TCFD Summit

October

IEA World Energy Outlook 2024 Release

BP Energy Outlook 2024 Release

Innovation for Cool Earth Forum (expected)

Connecting Green Hydrogen Japan 2024 (Oct 16-17)

Japan Wind Energy 2024 Summit (Oct 16-17)

Solar Energy Future Japan 2024 (Oct 16-17)

Japan Mobility Show (Oct 25-Nov 5)

November

US presidential election (Nov 5)

COP 29 in Azerbaijan (Nov 11-22)

Abu Dhabi International Petroleum Exhibition Conference (ADIPEC) 2024, Abu Dhabi, UAE (Nov 11-14)

APEC 2024 @ Lima, Peru

International Conference on Nuclear Decommissioning (TBD)

G20 Rio de Janeiro Summit (Nov 18-19)

Offshore Energy Exhibition & Conference (OEEC) 2024, Amsterdam, the Netherlands (Nov 26-27)

Biomass & BioEnergy Asia Conference (TBD)

European Biomethane Week 2024

December

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.