GX Promotion Act to take effect June 30; a boon for carbon trading and pricing, GX bonds, and more

Sales volume of new power suppliers down 21% in February; their total market share fell to the lowest in three years

JEPX to adopt a Belgian settlement calculation engine for its spot market; software already used in 26 European countries

ENERGY TRANSITION & POLICY

Perovskite solar tech added to national growth strategy

Japan to propose new CCS rules with Australia, ASEAN

EGC finalizes directives to the power utilities accused of cartel

ANRE to work on measures to limit renewable curbs by year’s end

Japanese investors warming to ‘transition bonds’

Mitsui to supply ammonia to JERA for co-firing trials in Aichi Pref

NEDO awarded funding for 32 hydrogen projects

Mitsubishi sets up company in Europe for green hydrogen

NRA chief, TEPCO execs meet on Kashiwazaki NPP security

ELECTRICITY MARKETS

J-Power in trouble over Oma NPP construction plans

Kansai Electric to restart Takahama Units 1 and 2 this summer

Akita offshore wind tender – Mitsui withdraws and Itochu joins

SSE Pacifico plans offshore wind power station in Tokushima

Global solar PV will reach 75 TW by 2050: AIST and partners

Blue Capital Management plans solar plant in Miyagi

Abalance and SPC connect solar plants, start selling electricity

NAC establishes Canadian subsidiary and acquires assets of NEP

OIL, GAS & MINING

JOGMEC seeks users of proprietary mining/ hydrogen tech

Mitsubishi invests in Marimaca Copper Project in Chile

Itochu and SKY Perfect begin oil spill monitoring service in Qatar

LNG stockpiles of power utilities increase again WoW

ANALYSIS

OIL REFINING INDUSTRY SEEKS ITS PLACE IN THE ENERGY TRANSITION

Thanks to energy efficiency, climate concerns and a shrinking population, Japan’s oil consumption declined by a third since 2000. Japan’s top three refining companies are now testing clean energy alternatives and pushing into new business areas to cut emissions and find revenue streams beyond oil. The main challenge is to transition and remain profitable. Japan NRG takes a look at how the domestic oil majors hope to reinvent themselves in a new green era.

LNG: A SUPER-CHILLED GAS THAT’S TOO HOT FOR BIG UTILITIES TO HANDLE

Since electricity retail was liberalized in 2016, LNG is a less attractive fuel for the major power utilities. METI has pushed the EPCOs to feed more volume into the wholesale power market, rather than selling directly to consumers. This has stimulated a vibrant power trading sector in Tokyo. However, it also turned gas-fired stations into a cumbersome asset class. The mismatch might see LNG futures contract trading take off. Or, it might lead to an even faster decline in Japan’s gas-fired generation.

New Energy and Industrial Technology Development Organization

kWh

Kilowatt hours (electricity generation volume)

TEPCO

Tokyo Electric Power Company

FIT

Feed-in Tariff

KEPCO

Kansai Electric Power Company

FIP

Feed-in Premium

EPCO

Electric Power Company

SAF

Sustainable Aviation Fuel

JCC

Japan Crude Cocktail

NPP

Nuclear power plant

JKM

Japan Korea Market, the Platt’s LNG benchmark

JOGMEC

Japan Organization for Metals and Energy Security

CCUS

Carbon Capture, Utilization and Storage

OCCTO

Organization for Cross-regional Coordination of Transmission Operators

NRA

Nuclear Regulation Authority

GX

Green Transformation

NEWS:ENERGY TRANSITION & POLICY

GX Promotion Act to take effect June 30

(Government statement, June 20)

The GX Promotion Act takes effect June 30, a week after its official proclamation.

CONTEXT: The Act introduces carbon trading and pricing, and GX state bonds to finance the transition to net zero. It passed the Diet in May. It lists 22 focus areas, ranging from ammonia/ hydrogen to batteries, to support via state and private financing. (See also “Japan’s New Emissions Trading System: Aiming High, but Going Slow” in the April 10, 2023 issue, and “Japan Unveils Energy Transition Roadmap but Nuclear Shift Grabs the Headlines” in Jan 16, 2023 issue).

TAKEAWAY: Some critics say the Act is about distributing funds to politically vocal sectors. However, the Act has the potential to be more effective than the Act on Promotion of Global Warming Countermeasures, which affirmed Japan’s 2050 net zero goal.

Starting in July, METI will set up several cross-industry and public-private sector frameworks to identify projects for financing and to craft common industry standards. As it seeks to catalyze Japan’s shift to new transition technologies, the Act will most likely lead to major changes in how businesses operate and develop.

EGC finalizes directives to power utilities accused of cartel

(Government statement, June 19)

The Electricity and Gas Market Surveillance Commission (EGC) finalized directives to power utilities accused of forming a price cartel. These were sent to the METI Minister, who has the power to issue administrative directives.

The directives address a cartel to restrain competition in business-user segments, which was exposed by the Japan Fair Trade Commission earlier this year.

Kansai Electric, Chubu Electric Miraiz, Chugoku Electric, Kyushu Electric and Kyuden Mirai Energy will be required to:

Establish cartel prevention measures and report these to the METI minister in writing;

set up an internal audit framework and an external audit panel;

conduct training, and etc.

CONTEXT: In March, the JFTC slapped the power companies mentioned above with ¥101 billion in total fines for violating the Anti-Monopoly Act. Only Kansai Electric avoided the fines due to leniency. The EGC issues administrative guidance based on the Electricity Business Act, and has no capacity to go after non-compliant companies.

SIDE DEVELOPMENT: Chubu Electric shareholders file damages claims (Company statement, June 21)

Six individual shareholders of Chubu Electric formally sent a request in writing to the company auditor to review the allegation that the company had violated the Anti-Monopoly Act and the damages this negligence and non-compliance caused. The shareholders calculate the damages at ¥37.7 billion.

TAKEAWAY: The antitrust charges against Chubu Electric and its affiliate Chubu Electric Miraiz totaled ¥27.4 billion, which is much less than the estimate made by the shareholders. That difference may become a discussion point.

ANRE to work on measures to limit renewable curbs by year’s end

(Government statement, June 21)

By the end of this year, ANRE plans to draw up measures that should decrease the curbs on renewables output.

Short term measures include:

reducing thermal power output,

generating power demand from storage batteries,

electrolysis equipment and heat pumps,

installation of power supply control units at network facilities.

Longer term measures are:

stronger area network interconnection,

using variable renewables as a means to adjust demand supply balance, and

re-balancing demand and supply through pricing.

CONTEXT: Renewable output curbs increased to 600 GWh in FY2022, from 100 GWh in 2018. ANRE forecasts recent power rate hikes to slow power demand growth, while at the same time output from renewables increases.

Japan to propose CCS rules with ASEAN, Australia

(Nikkei Asia, June 22)

Japan plans to propose common rules for CCS (carbon capture and storage) in tandem with Australia and Southeast Asian countries. The aim is to lead the deployment of CCS technology in the region.

The proposal includes shared metrics, safety criteria for storage facilities, and a monitoring process for leaks. This initiative is expected to lower operating costs and construction times for CCS facilities.

METI will present draft rules at the next Asia Zero Emission Community (AZEC) meeting, scheduled for June 24. The detailed proposal will be then discussed at the AZEC ministerial meeting next year. Japan is also considering providing technological support to ASEAN countries through JOGMEC.

TAKEAWAY: CCS, alongside other energy technologies such as hydrogen and ammonia generation, is one of the key components of the AZEC strategy towards decarbonization. Japan’s role in outlining clear CCS regulations, as well as technical support to ASEAN countries, is to further strengthen its energy leadership in the area.

SIDE DEVELOPMENT JAPEX, JGC, K Line, JFE Steel to conduct CCS studies in Japan, Malaysia (Japan NRG, June 19)

JAPEX, JGC Holdings, Kawasaki Kisen Kaisha and JFE Steel signed a MoU to launch carbon capture and storage (CCS) value chain studies. They will work with Malaysia’s PETRONAS to explore building international CCS value chains.

They will identify carbon storage sites in Malaysia, carbon capture and gas transport to the storage sites from the PETRONAS LNG complex in Bintu, and JFE Steel’s steelworks in Japan. Gas from Japan will be liquefied for marine transport.

This is JFE Steel’s first CCS project. Earlier this year, its rival Nippon Steel signed a MoU on CCS with ExxonMobil Asia and Mitsubishi.

CONTEXT: According to climate activist Kiko Network, JFE Steel’s Fukuyama and Kurashiki steelworks are Japan’s second and third largest emitting facilities, each releasing 18-22 million tons/ year of carbon.

TAKEAWAY: Regulatory and policy uncertainties cloud CCS’s outlook. Recently, state energy and metals resource development company, JOGMEC, presented an outline of how the CCS industry could develop in the country and the broader Asian region by the end of this decade, but Japan has yet to present regulations for the burgeoning sector. Transparent and clear rules will be needed to develop the above non-binding MoU into a legally binding business agreement.

Perovskite solar tech added to national growth strategy

(Government statement, June 16)

Perovskite (PSC) solar tech was added to the Kishida Cabinet’s national growth strategy – Grand Design and Action Plan for a New Form of Capitalism 2023.

The paper said in order to speed up implementation of PSC cells, the govt will push to innovate mass production technologies, stimulate demand and set up mass production systems. It will also support further the move from R&D to first installations and tests by end users.

CONTEXT: Currently, UK-based OxfordPV leads in PSC mass production after a launch in Germany this year. Its perovskite-on-silicon tandem cells recorded efficiency of over 28%, which is higher than conventional silicon cells. One of the founders, Dr. Henry Snaith, has cooperated with Dr. Miyasaka Tsutomu, the Japanese inventor of PSC.

TAKEAWAY: Presently, research institutes worldwide are competing to develop the highest PSC power efficiencies. The Japanese govt is aiming to change the game by being the first country to commercialize the tech on a massive scale.

The Solar Panel Reuse and Recycling Association asked METI to regulate unauthorized exports of used panels, to set standards on panel reuse, and to financially support inspection of used panels.

Panels without proper quality reviews have been shipped overseas and disposed of as industrial waste, the Association said.

Cluster-type wind turbines emerge as new energy source

(Nikkei, June 18)

Kyushu University’s Research and Education Center for Offshore Wind has developed a new turbine design featuring a shroud — a kind of wind-collecting “lens” — and plans to build a demonstration unit of 100 small wind turbines.

Theoretically, a multi-turbine system can generate more power than a traditional single-turbine unit of similar size, according to researchers.

Kyushu University and Riamwind, a Fukuoka-based startup spun off from the university, have joined in a project to build a demo system consisting of two turbine units, each with a diameter of 25 meters in 2024.

Data from this system will be used to build another comprised of a matrix of beams that support 100 turbines arranged in a 10-unit by 10-unit format. Measuring some 230 meters high and 280 meters wide, the system should have 20 MW of capacity.

CONTEXT: The output of a wind turbine grows in proportion to the swept parts of each turbine blade. This is why blades have grown increasingly larger over the years. The largest turbines currently in service are nearly 300 meters high, but enlarging their blades requires strengthening the tower on which they stand — a costly endeavor.

TAKEAWAY: Some experts say the cost-effectiveness of simply enlarging the blades for greater output is now approaching its limit. Large blades spin over 100 meters per second. When blades are spinning at such a high speed, even raindrops can damage them. And the noise emitted by huge, fast-spinning blades is also a problem.

Source: Riamwind

Japanese investors warming to ‘transition bonds’

(Nikkei Asia, June 19)

For the first five months of 2023, ESG bonds accounted for 26.5% of non-sovereign bonds issued in Japan, according to SMBC Nikko Securities. Transition bonds help to fund activities that support the issuer in the transition to net-zero carbon emissions.

Japan Airlines (JAL) issued transition bonds worth ¥20 billion, six times oversubscribed. The funds will go to purchase fuel-efficient jets. MHI is another firm issuing transition bonds to support carbon capture and hydrogen-fired turbines.

Despite the initial low acceptance of transition bonds, they’re gaining credibility as a tool to decarbonize energy-intensive industries. Transition finance was supported by the G7 in their communique after the recent Hiroshima summit and the Japanese govt is fully behind these financial instruments in its GX decarbonization strategy.

CONTEXT: Transition bonds are used to fund activities that support the issuer in the transition to net-zero. This category is still emerging and accounted for just 1.7% of ESG bond issuance in East Asia in 2022, said the Asia Development Bank. Japan’s transition plans also have holes to plug, such as the lack of specific reduction targets and timelines.

Ammonia co-firing most suitable to Japan: Analysts say

(Japan NRG, June 20)

Using ammonia for power generation is a good strategy for Japan, said several analysts speaking at a Refinitiv seminar on hydrogen and power. Japan and South Korea are the only countries that plan ammonia co-firing, while others plan to use ammonia for chemicals and hard-to-abate sectors.

Ammonia can be fed directly into power generation units, according to the webinar speakers, including an analyst from Refinitiv. Existing power and transmission infrastructure can be used, which cuts cost and time. Ammonia-fired generation could replace current thermal power plants that burn oil, gas or coal, and be a complementary source to variable renewable power sources.

Most of Japan’s coal power plants are less than 15 years old and are suited for co-firing.

Drawbacks include nitrogen oxide (NOx) emissions and fuel costs. Renewable power costs need to come down, and carbon storage space must soon be made available.

CONTEXT: One 1 GW coal plant with 20% ammonia co-firing will require 0.5 million tons/ year of ammonia.

TAKEAWAY: ANRE says NOx release for 20% ammonia co-firing can be controlled with present technologies. JERA is conducting a pilot 20% ammonia co-firing at the Hekinan Unit 4 thermal plant this fiscal year.

SIDE DEVELOPMENT Mitsui to supply ammonia to JERA for co-firing trials in Aichi Pref (Company statement, June 16)

Mitsui and JERA finalized an agreement for supply of ammonia fuel for co-firing trials at the JERA Hekinan Thermal Power Station in Aichi Pref.

Since FY2021, JERA has been conducting a demo project on the viability of large-scale ammonia co-firing at the Hekinan plant.

Mitsui will supply the ammonia fuel.

CONTEXT: With 50 years of expertise in the ammonia industry, Mitsui is a leading ammonia importer, handling up to 700,000 tons annually, mostly catering to Asia.

NEDO awarded funding for 32 hydrogen projects

(New Energy Business, June 19)

NEDO announced that it will support 32 projects in the hydrogen space. They are split into three categories: hydrogen utilization in local communities; fuel cells; and hydrogen supply chains.

The projects envision R&D work in the first two categories for three years through 2025. Work on supply chain building is expected to last five years through 2027.

Among participants chosen by NEDO are Aisin, Honda, Tokuyama, Mitsubishi, KHI, Kobe Steel, Okinawa Electric, Air Water, Toda Industry, AIST, Horiba, Toso, Riken, ENEOS, JERA, Nippon Shokubai, JGC, Chiyoda, Air Liquid, HySTRA, etc. and Universities of Tokyo, Kanazawa, Kyushu, Yamanashi, Hokkaido.

Among the projects selected are those that focus on:

Development of hydrogen production using SOEC with low-temperature waste heat at factories/business sites

Demonstration of stationary fuel cell power utilization for data centers

R&D into more efficient hydrogen fuel supply systems for regional markets

Development of hydrogen co-firing operations to regulating power supply in a commercial grid system

Construction of a combustion-type industrial furnace for decarbonization of a factory that mainly consumes heat

TAKEAWAY: There are too many projects and technologies to mention and clearly some are more niche than others. Still, it shows that there is a strong interest in the domestic industry to develop demand-side technologies for hydrogen. Ultimately, this will make or break the rise of the H2 economy. Without an adequate number of users / buyers, it’s hard to see the cost of producing or importing hydrogen declining. The timelines in this latest round of projects suggests that mass adoption of hydrogen technologies (in their various forms, including via ammonia) is seen as more realistic in the early 2030s.

SIDE DEVELOPMENT Mitsubishi sets up company in Europe for green hydrogen (Company statement, June 22)

Mitsubishi and its subsidiary N.V. Eneco set up Eneco Diamond Hydrogen (EDH) in Europe, which will develop green hydrogen and renewable energy projects.

EDH will leverage Eneco’s experience in renewables and MC’s industry network.

EDH will focus on the EU initially, but has plans to expand globally.

TAKEAWAY Experts have noted that the EU’s 2030 green hydrogen goals are hard to realize due to uncertainty in the regulatory framework, which hinders investments. Achieving these goals will be challenging unless national governments expedite authorization and provide financial assistance. Also, the lack of regulatory transparency and uncertain demand impede final investment decisions. Mitsubishi’s new company will soon face such challenges.

NRA chief, TEPCO execs meet on Kashiwazaki nuclear security

(Japan NRG, June 22)

NRA chairman Yamanaka met with TEPCO executives to improve security at the Kashiwazaki NPP.

The NRA had asked the company to set up surveillance teams and systems in the wake of problems with the lighting system in sensitive areas.

TEPCO said the systems will be set up in July.

The NRA will also assess TEPCO’s capability to run nuclear plants.

CONTEXT: In April 2021, the NRA ordered TEPCO to suspend operations at Kashiwazaki until it clears security standards. The site had other minor safety and security incidents, resulting in local ruling party leaders asking the central govt to set up a non-TEPCO entity to take over operations.

TAKEAWAY: There is a race against time at TEPCO to placate the NRA and become an operator of a working nuclear power generation facility again. The company’s official timeline sys that Unit 7 of the Kashiwazaki Kariwa site (1.35 GW) will be online in October. The NRA cares little for these deadlines and will likely ignore it. However, a decision on whether the station will run this winter or not will need to be taken within the next two to three months. This will significantly affect both Tokyo area power supply and TEPCO’s financials.

Mitsui Oil and Chevron to do pilot tests for new geothermal tech

(Company statement, June 22)

Mitsui Oil Exploration (MOECO) and Chevron will collaborate on pilot tests of an innovative geothermal tech known as advanced closed loop (ACL).

ACL utilizes underground loop wells to harness the power of heat and generate electricity by supplying water from the surface, eliminating the need for direct extraction of hot water or steam that’s traditionally done in geothermal power.

This novel approach has potential to significantly mitigate the challenges associated with conventional geothermal. The pilot will be held in Hokkaido’s Niseko region.

TAKEAWAY: Japan’s hot spring (onsen) industry opposes the development of geothermal power because it fears that extracting heat from the ground may cause a decline in water levels and temperatures at their facilities. Onsen owners argue that water sources, including hot springs, are fragile and vulnerable to overexploitation. New technologies that do not rely on direct extraction of hot water or steam, such as the one discussed above, may then convince the skeptical onsen industry.

A consortium of over 120 global companies, including Ford, as well as Japanese companies Honda, Nissan, and Mazda, have come up with draft standards for blockchain-based “battery passports” to track their environmental and social impact.

The EU plans to require such documentation for batteries starting 2026, and the U.S. and India are also considering the same. This will provide records of a battery’s supply chain, including material origin, recycled components, CO2 emissions.

Japanese companies Denso and Itochu are also part of the consortium. The rules, developed in collaboration with Amazon Web Services and Hitachi, will assign each battery an identification number using blockchain technology.

CONTEXT: Another consortium called Catena-X, which includes Volkswagen and Siemens, is also working on standards for battery passports. The push for battery passports is driven by environmental concerns and the need for economic security in the supply chain of industrially important metals like lithium and nickel.

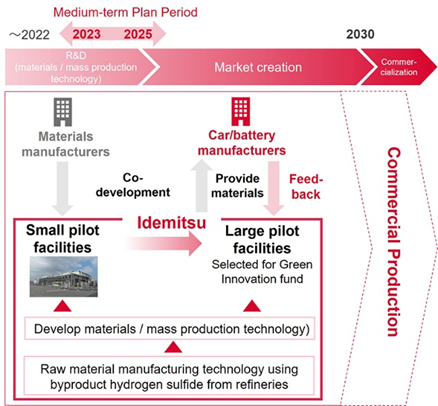

Idemitsu to increase supply capacity for all solid electrolytes for next-gen batteries

(Company statement, June 19)

Idemitsu will increase production capacity of solid electrolytes at its pilot plant in Chiba Complex to expand use of all-solid-state lithium-ion rechargeable batteries by late March 2024. From July this year, Idemitsu will start operation of another plant built within the Lithium Battery Material Dept in a different location of Chiba Pref.

The company sees the all-solid-state batteries as the technology to achieve longer cruising range, shorter recharging time, and improved safety for EVs. By utilizing samples produced from the two plants, Idemitsu will establish mass production technology and scale up for commercial production.

R&D will be done in association with Idemitsu’s R&D organizations in Switzerland, South Korea, and the U.S. This project is financed by the Green Innovation Fund from NEDO, and Idemitsu aims to start commercial production in 2027.

Researchers tout methane-eating bacteria in cutting rice farming emissions

(International Journal of Systematic and Evolutionary Microbiology, 2023)

Researchers led by Prof. Asakawa Susumu of Nagoya University studied a new bacteria species in rice paddy fields that oxidizes methane and cuts its release.

Methylocystis Iwaonis grows by absorbing methane and carbon as energy sources and oxidizes the gasses. It was sampled in the soil of rice paddy fields in Aichi Pref.

CONTEXT: Rice growing generates 20-30 million tons/ year of methane globally. Water management is the main emission reduction tech, by as much as 25%.

TAKEAWAY: Scientists knew about the bacteria for decades but it did not have a name until recently. Research on natural methane cuts without major environmental impact is still premature, but if developed it could diversify methane reduction techniques in food chains.

Chubu Electric began talks about waste incineration, methanation, and biomass power

(New Energy Business, June 20)

Chubu Electric agreed with the city of Hekinan, Aichi Pref for material recycling including construction and operation of an incineration plant, and local generation and consumption of biomass energy.

Hekinan city has been incinerating garbage at the Clean Center Kinu-ura. The local govt plans to use methanation from biomass as a pre-treatment to reduce the volume of garbage, and even generate electricity out of those wastes.

The Clean Center Kinu-ura can process 190 tons/ day of garbage. Hekinan and Takahama are responsible for operation and management of the center.

JAL signed purchase agreement with Shell for SAF in Los Angeles

(Company statement, June 16)

Starting 2025, Japan Airlines (JAL) will refuel aircraft with sustainable aviation fuel (SAF) in Los Angeles sourced from Shell Aviation to replace 1% of its jet fuel.

JAL will use fuels that emit 75% less CO2 than conventional jet fuels. Replacement with SAF will rise to 10% by 2030.

NEWS:POWER MARKETS

Sales volume of new power market entrants drops 21% in February

(Denki Shimbun, June 22)

According to the Electricity and Gas Market Surveillance Commission, the total electricity sales volume in February was 7,284 million kWh, a decrease of 7.8% YoY, and down 4.9% compared to the previous month.

The breakdown is as follows: Sales by all electricity retailers decreased by 4.2% YoY to 5,917 million kWh, and down 4.9% over the previous month.

New power suppliers (shin denryoku, or the new entrants to the power market since 2016) saw sales decline for the fifth consecutive month, down 21% to 1,367 million kWh, and down 5.1% over the previous month.

Regarding the share of new power suppliers in the sales volume in February, it was 18.8%, a decrease of 3.1 percentage points YoY.

TAKEAWAY: This is the lowest market share that new market entrants have had since at least 2020. The major power utilities saw their market share erode since 2016 to less than 78% at one point. In the last 18 months, due to wild swings in fuel and electricity prices, many new suppliers have withdrawn from the market or stopped taking on new customers. This has helped the EPCOs, which have nonetheless also struggled to stay profitable in the current environment.

JEPX (Japan Electric Power Exchange) will adopt a settlement calculation engine for its spot market, provided by N-SIDE, a Belgian software company.

This software is already in use in 26 European countries. N-SIDE plans to open an office in Tokyo.

N-SIDE’s settlement calculation engine is based on the optimization calculation method called “EUPHEMIA” that was developed for the common European spot market.

JEPX’s current system verifies block bids one by one according to predetermined procedures to confirm whether they are settled. By introducing optimization calculations, JEPX will be able to determine the optimal combination of blocks to maximize the execution volume. This will make trades faster and more efficient.

CONTEXT: In Europe, about 40% of the electricity sales are traded in the spot market.

Ryoichi Kunimatsu, General Manager of JEPX’s Planning and Business Department, said that using a settlement calculation engine that can handle complexities will enable accurate responses even if the Japanese market becomes more intricate.

J-Power in trouble over Oma NPP construction

(FACTA, June edition)

J-Power (Electric Power Development Co) admitted errors in the safety review of the Oma Nuclear Power Plant in Aomori Pref, which has halted progress.

The company mistakenly entered the distance from a hypothetical fault (F-14 fault) to the surface as “3m” instead of the correct “3km”.

J-Power was warned to check seismic data during an NRA hearing in February 2022, but dismissed the concerns.

The seismic analysis work was subcontracted to four companies, and when J-Power asked a new company to check the analysis of the F-14 fault due to the persistent request of the regulators, the input error was discovered in January.

TAKEAWAY: Oma NPP is designed to be the world’s first full MOX (Mixed Oxide fuel, a blend of plutonium and uranium) commercial reactor, with one of the largest capacities in Japan, at 1.38 GW. Construction began in 2008, but was suspended after the Fukushima disaster in 2011. The project’s start date, initially set for 2012, has been pushed to 2030. A full suspension of this project could spell the end of J-Power’s ambition to become a nuclear power utility, but it’s unlikely that the govt will let the company flounder.

KEPCO to restart Takahama Units 1 and 2 this summer

(Company statement, June 21)

Kansai Electric announced its new timeline for the restart of Units 1 and 2 of the Takahama NPP.

Unit 1 goes online on June 22, with load performance test and resumption of full operation by late August. Unit 2 restart is set for early August with full operation slated for mid-Oct.

TAKEAWAY: The restart would be a fairly significant landmark for the nuclear sector since it could bring all of Kansai Electric’s seven units into operation. Takahama NPP Units 1 and 2 are among the oldest reactors currently certified to operate in Japan. So far, the utility reported that it has safely loaded all of the uranium fuel rods into Unit 1.

Akita’s second round for offshore wind – Mitsui withdraws and Itochu joins

(Diamond, June 20)

Mitsui will withdraw from a wind tender in Akita, where it partnered with Northland Power (Canada) and Osaka Gas. Since tender rules changed and the govt introduced “Zero Premium Standard,” Mitsui decided the project won’t be profitable.

After Mitsui’s withdrawal, Itochu joined JERA and J-Power’s group. Itochu plans to participate in future offshore wind projects, and this Round 2 project experience will help.

Here are four groups that will participate in the Akita offshore tender.

Cosmo, JAPEX, Venti, Shimiz

JERA, J-Power, Itochu

TEPCO, Orsted

Marubeni, Tokyo Gas

SIDE DEVELOPMENT SSE Pacifico plans offshore wind station in Tokushima Pref (Company statement, June 16)

SSE Pacifico will build a wind power station off the coast of Minami-cho in Tokushima Pref. The environmental assessment will be on its website until July 18.

The station has a 30 MW total capacity, sourced from 3 wind turbines. It anticipates an average of 7 meters/ second of constant wind, with less frequent (marine) traffic.

KEPCO and JR West agree on PPA and renewable energy supply

(Company statement, June 19)

KEPCO and West Japan Railway (JR West) announced a PPA and renewable energy supply agreement for the Osaka Loop Line and JR Yumesaki Line.

JR West will reduce CO2 emissions by about 32,000 tons per year. Under the PPA, JR West will purchase electricity from solar power facilities with 5.5 MW total capacity.

The remaining electricity needed for the operation will be supplied via the “Renewable Energy ECO Plan”, which includes procuring and providing non-fossil certificates of renewable energy origin.

AIST, NREL, and Fraunhofer say global solar PV will reach 75 TW by 2050

(New Energy Business, June 16)

Japan’s National Institute of Advanced Industrial Science and Technology (AIST), the National Renewable Energy Laboratory (NREL) in the U.S., and Fraunhofer Society in Germany published a paper, “Photovoltaics at multi-terawatt scale: Waiting is not an option”, which summarized their discussions during the workshop in May 2022.

The paper states that 80% of newly installed energy in 2022 comes from renewables, and solar PV reached 1.1 TW at the end of 2022. Solar PV only accounts for a 4-5% share of total electricity today, but with a CAGR of 25%, capacity doubles every three years. It will reach 3.4 TW in 10 years, and 75 TW by 2050.

Solar PV is seen as a relatively cheap way of growing renewable energy capacity.

Blue Capital Management plans 51 MW solar plant in Miyagi

(Company statement, June 16)

Blue Capital Management published its environmental assessment for a 51 MW solar power project in Sendai, Miyagi Pref, to be located at a former golf course.

The company will install 78,450 units of solar panels; each generates 650 W of electricity. Construction starts in January 2024; completion is expected in December 2025. The assessment is open to the public until July 18.

Abalance and SPC connect solar plants, start selling electricity

(Company statement, June 14)

Abalance, and its subsidiary SPC, connected to the grid two solar power plants (each 11 MW capacity) and began providing electricity in Miyagi Pref.

The companies expect revenue of ¥470 million in the first 12 months of operation.

The solar farms are in Taiwa town and Oohira village.

NAC International establishes Canadian subsidiary and acquires assets of NEP

(Company statement, June 19)

NAC International, a Hitachi subsidiary specializing in nuclear fuel and radioactive materials management, established a Canadian subsidiary called Niagara Energy Products (NEP) and acquired its assets.

NEP is a leading producer and supplier of nuclear containers for safe handling of radioactive waste.

The acquisition allows NAC to serve the Canadian nuclear market. NEP will offer integrated nuclear waste management solutions to customers.

Juwi Shizen Energy forms operation monitoring center in Miyagi

(Company statement, June 19)

Juwi Shizen Energy Operation (JSEO) founded an operation monitoring center in Sendai, Miyagi Pref to monitor renewable energy power generation plants, 24 hours a day and 365 days a year. Whenever a failure occurs at a plant, trained service staff will rush to the site to solve the problem.

The monitoring system was introduced at the 147 MW Onikoube Solar Power Station in Osaki, Miyazaki Pref where JSEO does O&M. It’s located in an area with heavy snowfall in winter, and quick action is needed to remove snow to maintain consistent power generation efficiencies.

JSEO will save the data from monitoring its plants, and utilize it to expand into storage battery monitoring for the grid.

Azbil and KEPCO collaborate on equipment abnormality detection with AI system

(Company statement, June 19)

Azbil Corp and KEPCO developed an AI-based abnormality detection system. They’ll implement this system in thermal power plants and large factories.

Azbil has expertise in AI development; KEPCO knows thermal power plants.

This system automates AI model construction, allowing for a wide range of data inputs. It can monitor a larger area and identify anomalies previously unnoticed.

On July 27, JOGMEC will hold an online presentation of its proprietary mining, hydrogen/ammonia production and other technologies, inviting cooperation from the private sector, including technology licensing.

The presentation covers AI-assisted mining, recovery of rare metals from copper ores, carbon-derived absorbent materials for hydrogen and ammonia production, etc.

Mitsubishi invests in Marimaca Copper Project, Chile

(Company statement, June 22)

Mitsubishi inked an agreement with Canadian-owned Marimaca Copper, and will invest C$20 million in a private placement to buy about 5% of its common shares.

The Marimaca Copper Project in north Chile was discovered in 2016. The project aims to produce 50,000 tons of copper cathode per year for at least 15 years.

Production will begin by around 2030.

Itochu and SKY Perfect begin oil spill monitoring service in Qatar

(Company statement, June 19)

Itochu and SKY Perfect JSAT announced the launch of a service that uses Synthetic Aperture Radar (SAR) to detect oil spills for Qatar’s Ministry of Environment.

The service combines SAR satellite imagery and Automatic Identification System (AIS) data from vessels to identify and locate offshore oil leaks. This is the first time the two companies offer satellite-based analysis services outside of Japan.

The service aims to protect critical coastal facilities such as desalination plants and power plants from oil leak damage.

LNG stocks of 10 power grids stood at 2.37 million tons as of June 18, up 2.6% from 2.31 million tons a week earlier. METI first reported the June 11 stocks at 2.3 million tons but revised the figure.

The end-June stocks last year were 2.14 million tons. The five-year average for this time of year was 1.95 million tons.

ANALYSIS

BY KYOKO FUKUDA

Oil Refining Industry Seeks its Place in the Energy Transition

Sales of electric vehicles (EVs) globally have more than tripled in the last two years and accounted for over 20% of all car sales in major markets like China and Europe. In Japan, the shift to battery-only EVs has been slower, but the future of cars powered solely by fossil fuels is clearly limited, especially as more governments pass laws mandating an end to their sales.

How much petroleum products we’ll continue to consume over the coming decades is still the subject of much debate. But there’s a concerted push across road, air and sea transport to move away from crude oil-based fuels. Japan’s oil-fired generators are largely slated for decommissioning, and the nation’s 2050 carbon neutrality goal is now enshrined in law.

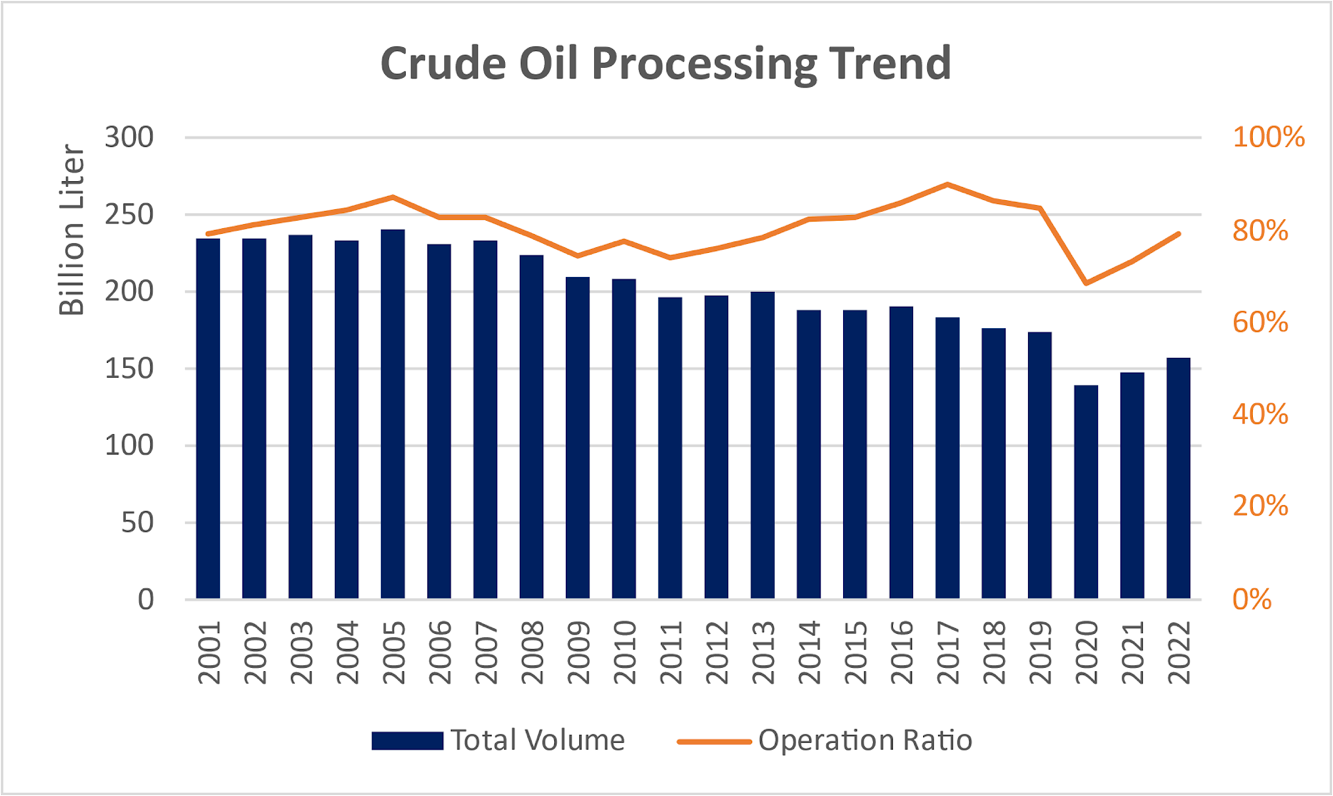

Thanks to better energy efficiency, climate concerns and a shrinking population, Japan’s oil consumption has declined by a third since the turn of the century. There are still 21 active refineries, capable of processing about 3.3 million barrels/ day, but within five years these operations will be subject to a new carbon levy that the government wants to help pay for a ¥150 trillion national decarbonization program, the GX.

As far as the oil refining companies are concerned, they’ve seen enough. Japan’s top three refining companies are now actively testing clean energy alternatives and pushing into new business directions to reduce their total emissions and find revenue streams beyond oil. The main challenge for the sector, however, is to transition in such a way as to remain profitable.

Japan NRG takes a look at how the domestic oil majors hope to reinvent themselves in a new green era.

Company

Refinery Name

Location (Pref.)

Production Capacity

(Barrels/day)

Idemitsu Kosan

Hokkaido

Hokkaido

150,000

Chiba

Chiba

247,000

Aichi

Aichi

160,000

Toa Oil

Keihin

Kanagawa

70,000

Seibu Oil

Yamaguchi

Yamaguchi

120,000

ENEOS

Sendai

Miyagi

145,000

Kawasaki

Kanagawa

247,000

Negishi

Kanagawa

150,000

Sakai

Osaka

141,000

Wakayama

Wakayama

120,400

Mizushima

Okayama

350,000

Marifu

Yamaguchi

120,000

Ooita

Ooita

136,000

Kashima Oil

Kashima

Ibaraki

203,100

Osaka Kokusai

Chiba

Chiba

129,000

Cosmo Oil

Chiba

Chiba

177,000

Yokkaichi

Mie

255,000

Sakai

Osaka

100,000

Fuji Oil

Sodegaura

Chiba

143,000

Showa Yokkaichi Sekiyu

Yokkaichi

Mie

255,000

Taiyo Oil

Shikoku

Ehime

138,000

Kashima Oil and Osaka Kokusai belong to ENEOS Group.

In the past 20 years, Japan’s crude oil imports and processing volume have decreased by nearly 30%. In FY2022, Japan imported about 156 billion liters of crude oil, mainly from the Middle East, and processed 3.4 million barrels per day. Refineries’ operating rate was 79.2%.

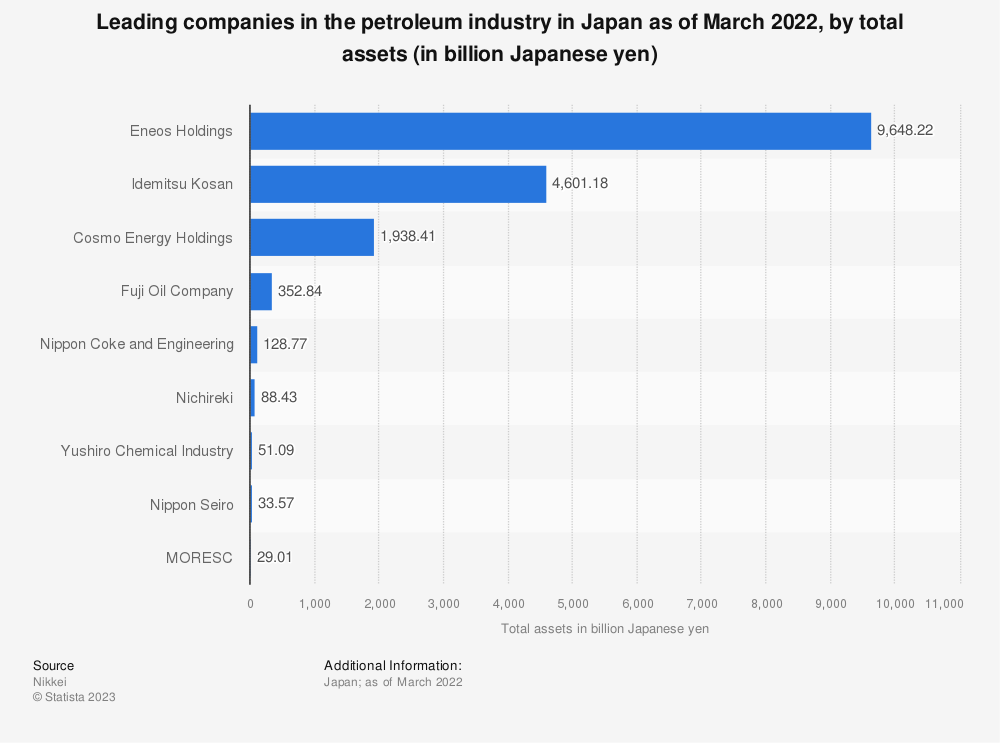

Japan’s largest oil company is ENEOS, with group sales of ¥15 trillion in FY2022 and profit of ¥281.3 billion. Founded in 1888 as Nippon Oil, ENEOS has pledged to reduce 1.5 million tons of CO2 (Scope 1 and 2) compared to FY2009, with an additional reduction of 1.2 million tons (Scope 3) in its supply chains.

Eager to find its place in the future energy landscape, ENEOS is investing heavily in renewable energy such as solar, wind, and biomass power generation. In January 2022, it acquired one of the domestic solar industry pioneers Japan Renewable Energy Corporation (JRE), adding 82 renewables sites to the group’s own biomass, solar and wind assets.

ENEOS also promotes hydrogen energy and has installed 47 hydrogen refueling stations nationwide. Among other R&D directions are ways to reduce CO2 emissions from the company’s fossil-based products such as kerosene, lubricants, etc.

One of ENEOS’ most ambitious projects is sustainable aviation fuel (SAF). By 2030, Japan intends to replace 10% of national jet fuel consumption with SAF. In April 2022, ENEOS submitted to METI its plan to produce SAF, in cooperation with TotalEnergies. Their original idea was to convert the Negishi refinery into a SAF production facility with an annual capacity of 400 million liters. In November 2022, the plan was modified to utilize the Wakayama refinery. First production is now expected in 2026, a one-year delay.

In March, ENEOS joined forces with AMPOL Australia Petroleum, the country’s largest petrol supplier, to produce biofuel in Australia. Their goal is to develop production with an annual capacity of 500 million liters of SAF and establish a Japan-Australia SAF supply chain.

The government expects Japan’s domestic SAF demand to be in the range of 2.5 to 5.6 billion liters by 2030, and 23 billion liters by 2050. So far, however, only about 63 million liters or 0.03% of global demand is serviced with SAF.

As with nearly every area of the energy transition, the main sticking point is cost. SAF production carries costs that are two to 16 times higher than conventional jet fuels. The hope is that R&D and more innovations will bring down costs. But that hope remains ambiguous.

Cosmo Oil

Cosmo Oil was established in 1986 by merging Maruzen Oil, Daikyo Oil, and Cosmo Oil. Total sales in FY2022 were ¥2.8 trillion with profit of ¥67.9 billion attributable to owners of the parent company. Similar to ENEOS, Cosmo aims to reduce its CO2 emissions, as stated in its plan for 2018-2022. In 2021, Cosmo emitted 490,000 tons of CO2 less than in 2013.

Over the coming decade, Cosmo’s strategy for carbon neutrality calls for wider use of LNG (instead of dirtier fossil fuels like coal) and a shift to biofuels, hydrogen, ammonia, and low emission materials. Also, Cosmo wants to deploy more CO2-Enhanced Oil Recovery (EOR) technology to increase the recovery factor of crude oil, claiming that this too is a way to lower overall emissions from the sector by recycling CO2.

Cosmo is also keen to tap the potential of wind. In 1996, Cosmo was among the first movers into wind generation in Japan when it installed two 400 kW wind turbines in Yamagata. It is now building wind farms under the brand name of Cosmo Eco Power. So far, Cosmo has installed 149 wind turbines across Japan with a total capacity of 308 MW. Cosmo hopes to win some tenders in the offshore wind space, and has set itself the goal of assembling 1.5 GW of wind power capacity by 2030.

Recently, Cosmo also added the SAF business to its 2030 strategy. It aims to start commercial operations in the sector by 2024/25 when it could supply as much as 30 million liters of SAF. The volumes could rise to 300 million liters by 2030.

This May, Cosmo began building its first SAF production line at the Sakai oil refinery. It will process waste cooking oil from restaurants and other facilities and blend it with regular fuel. The Sakai facility also produces bio-naphtha and renewable diesel for bio-plastics.

In the SAF business, Cosmo will work with JGC (an engineering firm with SAF production technology), Revo International (as the collector of SAF raw materials), and Saffaire Sky Energy (SAF consumer). Cosmo and JGC have set up a JV to run the business in which they each own 48%.

To hedge its bets, Cosmo is exploring another SAF production process with trading house Mitsui & Co. The two companies are mulling setting up production of 220 million liters of ethanol-based SAF by 2027 with no factory location decided so far.

Idemitsu, Japan’s second largest oil refiner, was founded in 1911 selling lubricant oils. The company’s sales in FY2022 were ¥6.7 trillion, with a profit of ¥434.5 billion. In November 2022, Idemitsu announced its mid-term business plan for 2023-2025, including a 2050 decarbonization strategy.

Idemitsu intends to build a carbon neutral energy supply chain around green hydrogen, ammonia, and other synthetic fuels. It also wants to establish a plastic recycling system; shift from petrochemicals to bio-chemicals; establish EV and Li-ion battery businesses; and expand its renewable energy business and solar panel recycling.

Idemitsu owns 1.8 GW of power generation, of which 700 MW is renewables.

Currently, 95% of the company’s profit comes from fossil-fuel-related businesses, but the goal is to reduce that to 70% by 2025, and 50% by 2030. This transition includes shutting down Seibu Oil’s refining facilities and integrating Toa Oil as a 100% subsidiary. The Tokuyama factory in Yamaguchi Pref has already stopped refining, and will be turned into a terminal to import ammonia in the late 2020’s. The location’s LPG tanks might be used as ammonia storage tanks.

At first, Idemitsu wants to focus on bringing more new energy businesses to a commercial scale and profit, hoping for a return on invested capital (ROIC) of 7% in 2030. By the 2040s, the company expects that its primary business profile will be in carbon-free ammonia, carbon-free hydrogen, synthetic fuels, and carbon capture, utilization and storage (CCUS).

Like its domestic rivals, Idemitsu has big expectations for the SAF business. It plans to start producing 100 million liters of SAF at the Chiba refinery by 2026, and expand that with another 500 million liters of capacity across several facilities by 2030.

Of the nine main SAF production processes known today, Idemitsu seems to prefer alcohol-to-jet (ATJ) and hydroprocessed esters and fatty acids (HEFA), followed by cellulosic fuels. Idemitsu wants to import bioethanol for raw materials to produce SAF utilizing existing terminals and tanks.

In terms of investments, Idemitsu has set aside ¥290 billion for establishing new businesses in the next three years, which is close to half of its total ¥690 billion budget for the period.

No quick solution

The general consensus is that the oil refining business will be around for another 30 years at least, but there is little consensus around the size of that business in the coming decades. It makes sense for Japan’s refining majors to start laying foundations for the future.

The difficulties they face are the relatively low ROIC in new energy sectors such as solar or wind power generation, and the high costs associated with new fuels such as hydrogen and its derivatives. Here is where government regulation may help.

METI is planning to mandate that all international flights arriving in Japan use at least a 10% SAF blend. That would create a ready market for the oil refiners, which will surely look to the state to provide similar support elsewhere.

ANALYSIS

BY JAPAN NRG TEAM

LNG: A Super-Chilled Gas That’s Too Hot for Big Utilities to Handle

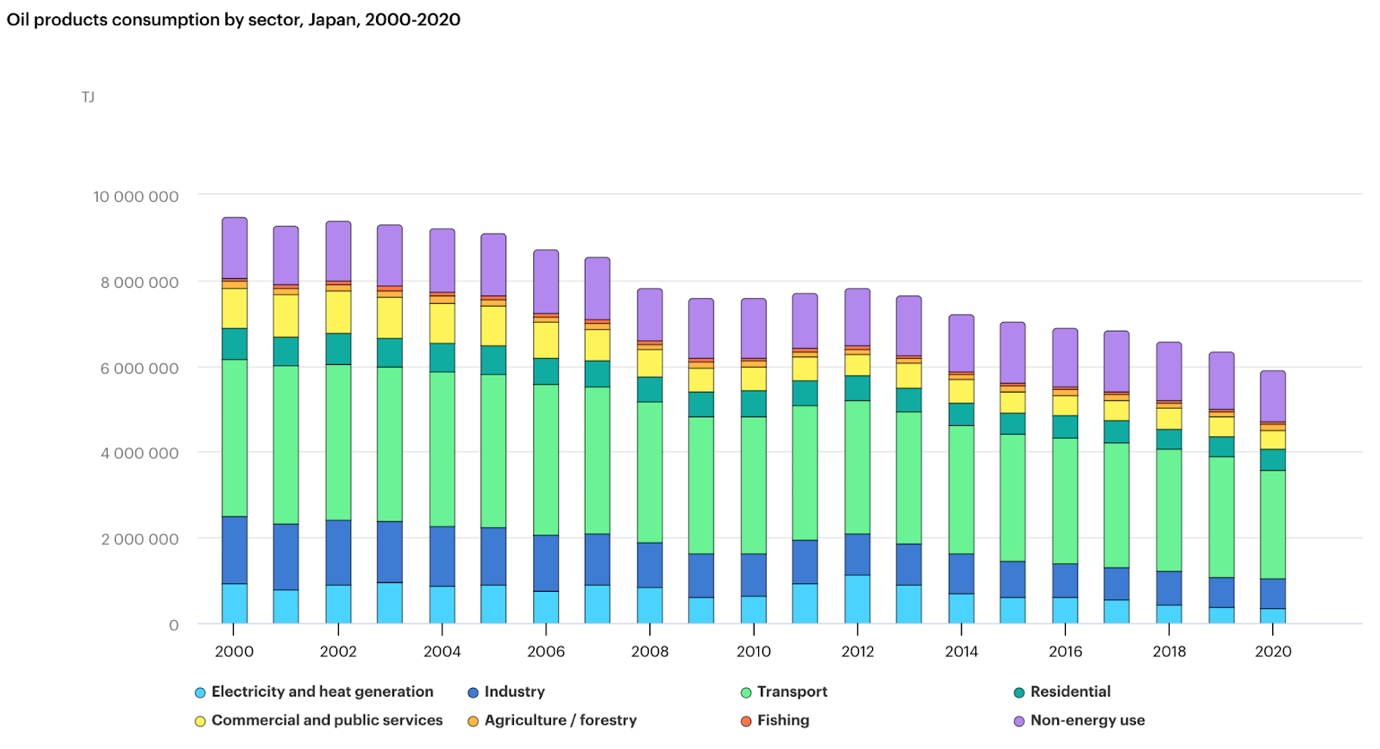

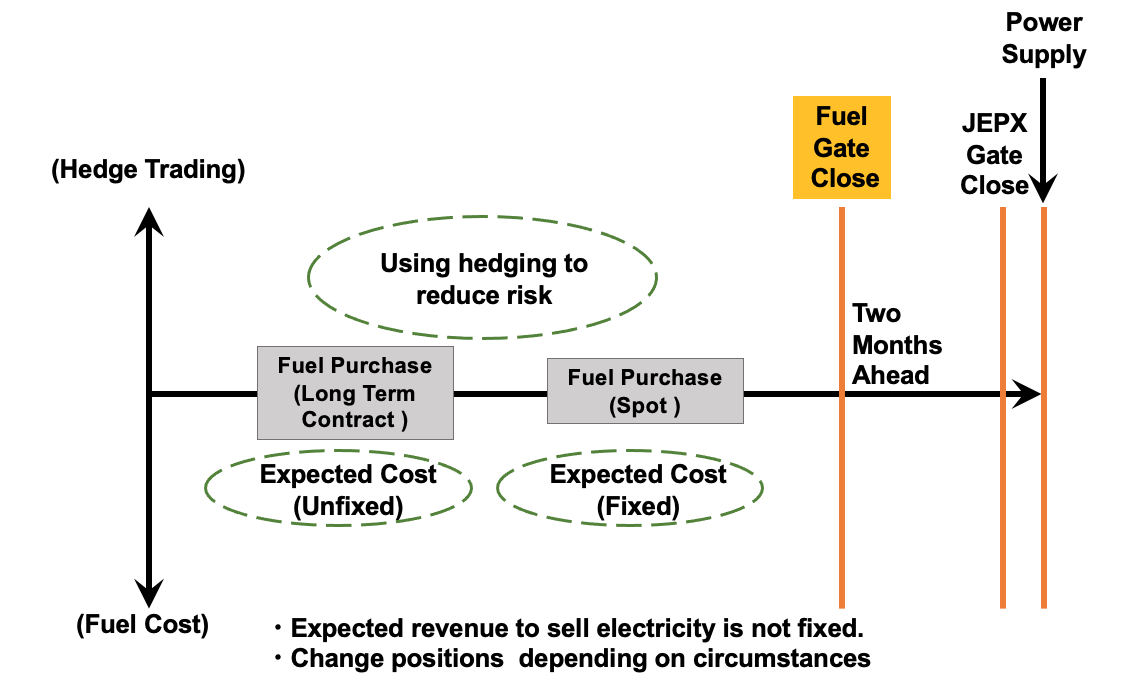

In the last five years, Japan’s LNG imports have been on the decline. The reasons often cited are LNG’s cost, the restart of nuclear capacity, and, of course, climate action. However, there’s one other factor diminishing Japan’s appetite for the super-chilled fuel: liberalization of the power market.

Since electricity retail was completely opened up in 2016, the market dynamics have changed. In addition to fostering competition in generation, METI used the 2016 reform to push the big utilities (EPCOs) to feed more of their volumes into the wholesale power market, rather than selling directly to consumers. This has stimulated a vibrant power trading sector in Tokyo. However, it has also made gas-fired stations a more cumbersome asset class.

Put simply, the fuel for an LNG-fired power plant must be secured at least two months before it’s burned to produce electricity. In contrast, in a system where a significant volume of electricity is sold on an exchange, the (almost) fixed level of power demand only becomes clear a day before. That’s not enough to significantly adjust the operations of a thermal power plant. But while coal and oil can be kept in reserve for another day, Japan’s LNG storage options are limited and very short term. Thus, any gas fuel surpluses or shortages become a cost burden.

Keen to protect energy security, the government is trying to find solutions. Among them is a strong push for electricity market participants to embrace power derivatives. Another is a ploy to bring greater transparency to wholesale power trading.

Whether these will be enough, however, is unclear. The mismatch may finally see LNG futures contract trading take off in Tokyo. Or, an even faster decline in Japan’s gas-fired generation.

Changing fundamentals Japanese LNG import volumes are down almost 14% in the last five years, but the nation still ranks as the top global buyer, with 72 million tons shipped to Japan in 2022. However, the pace of decline is accelerating. The volumes for the first four months of this year are 15% less than the five-year average for the same period.

There are many factors behind this. One is the mild revival in nuclear generation. Japan has nine reactors online today, several units more than a few years ago. Still, online nuclear plants are limited to just three regions: Kansai, Shikoku and Kyushu.

Recent crises, especially in January 2021 when there was trouble with delivering LNG cargoes to Japan, made LNG the most volatile of the major power fuels over the last three years. Also, its price hit hitherto unimaginable levels in 2022 after sanctions against Russia upended global energy markets.

In addition, the global LNG market remains tight; geopolitics means that future supply of Russian LNG to Japan is uncertain; and investments in future upstream and midstream projects often run up against climate considerations.

Japanese utilities have reported plans to decommission over 26 GW of gas-fired capacity in the next ten years or so. While there are also plans to build new units, which should make the net decline much smaller, the drop is still significant. It also aligns with the latest Basic Energy Strategy that forecasts a halving of gas-fired generation in the nation’s power mix by 2030.

EPCO perspective

From the viewpoint of big power utilities, gas generation is less attractive than it once was. While GHG emissions from burning LNG are nearly half that of coal, when it comes to flexibility the latter offers more latitude even before global market fundamentals are considered.

Since 2016, METI has rolled out a number of power trading platforms to mirror changes in the competitive landscape. The key one is the JEPX wholesale electricity trading exchange, also known as the spot market.

It operates on a day-ahead basis, which means that demand becomes clear only a day earlier, based on plans submitted by retailers for the following 24 hours. The time between when a plan is submitted and the actual delivery of electricity is known as “Gate Close”.

Source: METI

The majority of LNG volumes are secured on long-term contracts that run for a decade or more. Even when sourced on the spot market, it takes several months to contract an LNG delivery and agree terms. In Japan, the minimum time between securing the fuel and when it is used, as per the reporting process to METI, is two months. That period is known as the “Fuel Gate Close”.

Before electricity market liberalization, EPCOs were responsible for all power generation and delivery. That allowed them to plan which power stations to deploy at what time and for how long. Adjustments could be made without significant loss, since all of the assets belonged to the same company, which also balanced and transmitted the power.

In today’s electricity market, EPCOs only have an 80% share of sales. Plus, the grid operations are supposed to be neutral and, in times of surplus, in favor of renewables generation. That does not bode well for EPCO’s mostly thermal power plants and leaves the big utilities with much less room for internal adjustment to operations.

What makes the issue more poignant is that the EPCOs can’t store LNG for more than two weeks. Unlike Europe, Japan doesn’t have underground gas storage due to a dearth of used gas fields and unsuitable geology. Also, there are no direct pipeline links to other countries, which might allow for minor adjustment in volumes, and no centralized gas pipeline network to move the fuel around the country as a balancing tool.

The additional electricity trading platforms, such as the Balancing Market, are not considered deep or liquid enough to cover the mismatches. In the end, the financial losses that come with buying too much or too little LNG are borne by both generators and eventually retailers, which translates into higher electricity prices for consumers.

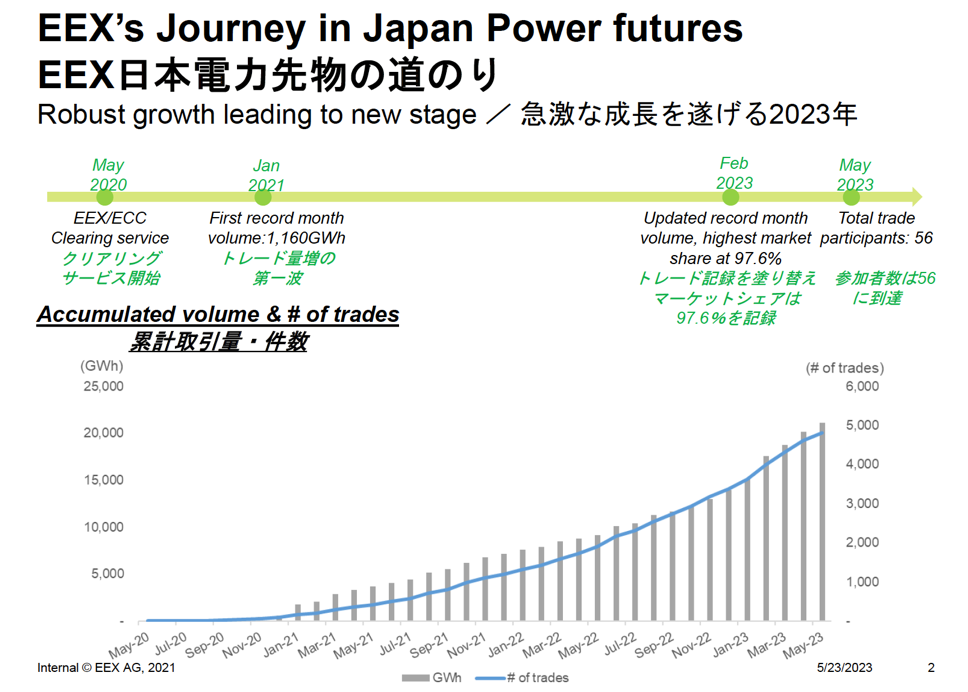

Solutions One way to avoid losses would be through futures contracts. That’s one reason METI has vigorously pushed all power retailers to embrace risk-hedging in the derivatives market. The two major platforms in Japan are the EEX and TOCOM.

EEX, which hosts around 90% of the electricity futures trading in Japan, reported a rapid rise in trading volume and market participants in the past two years, and especially in the last six months.

Source: EEX

EEX had record trading volumes in February 2023. The volume in the first five months of this year (7,632 GWh) has already surpassed last year’s total (6,745 GWh).

Still, even with such rapid growth, Japan’s ratio of futures trading compared to the spot wholesale market (JEPX) is only about 6.7% on a year-to-date basis, according to EEX. In mature power markets, the derivatives volume is several times bigger than the physical volume.

To promote the adoption of power futures by market participants, METI plans to start disclosing how much retailers are using hedging tools. That would make clear which retailers are making the most effort to stabilize electricity prices, according to the logic of state officials.

There’s another lever the ministry has in mind. Starting 2025, METI will mandate retailers to submit data to OCCTO to demonstrate how dependent they are on buying electricity on the spot JEPX market (as opposed to meeting their customer contract obligations via own generation facilities). The ministry believes that collecting data on retailers’ JEPX reliance will bring more transparency to the industry and help all stakeholders.

LNG derivatives to take off?

The other end of the stick would be to hedge the risks that EPCOs take in buying LNG fuel through a derivatives market. TOCOM, now part of the Tokyo Stock Exchange, launched yen-denominated LNG contracts in spring of 2022. The cash-settled derivative is purely a financial instrument with no link to physical delivery of LNG.

The timing of TOCOM’s offering was unfortunate. With markets in crisis mode after Russia’s incursion into Ukraine, LNG supply, prices and logistics were thrown into turmoil. This made the financial instrument too hot to handle.

The demand for hedging LNG risk, however, was clearly there. Later in 2022, Tokyo-based energy marketplace operator enechain Corp offered to create a pooling system through which smaller power retailers could band together and purchase the equivalent of one LNG cargo. Enechain sees interest in such an aggregate system, but admits that it would still hedge only a small portion of the LNG volumes that Japan imports.

From the government’s standpoint, larger solutions are required. As METI promotes the wider use of electricity futures, officials will find it convenient to support the emergence of a similar market in LNG. If not, EPCO’s interest in maintaining a sizable LNG-fired asset base will wane.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

China/ Oil demand

The world’s top crude importer will see demand grow this year, but less than expected due to increased EV sales. The country’s oil demand will reach 743 mmt this year, equivalent to around 15 mbpd. In 2019, that figure was 10 mbpd.

Germany/ LNG imports

State-owned SEFE signed a 20-year deal to import 2.25 million tons of LNG annually from Venture Global LNG on the Gulf of Mexico. The companies did not disclose the price of the deal, but U.S. gas is much more expensive than Russian supplies.

New York/ Grid modernization

Grid operators plan the $3.3 billion Long Island transmission project to bring 3 GW of offshore wind energy to the state. However, that still won’t accommodate the 2035 target of 9 GW of offshore wind energy.

Qatar/ LNG deal

China National Petroleum Corp signed a 27-year deal with QatarEnergy to purchase 4 million tons of LNG. CNPC will also take a 5% stake in Qatar’s expansion project in its North Field, the world’s biggest natural gas reservoir.

South Africa/ Green hydrogen

South Africa, Netherlands and Denmark launched a $1 billion green hydrogen fund. South Africa’s energy transition envisages setting up an ecosystem and export hub for green hydrogen. President Ramaphosa said this requires $17 billion.

Texas/ Permian basin

Civitas Resources will acquire oil and gas operations in the Permian Basin managed by NGP Energy Capital for $4.7 billion. High inflation and greater focus on investor returns limited shale growth last year, but in 2023 shale oil supply is expected to grow.

Ukraine/ Energy grid

Ukraine will make major repairs to its power system to prepare for another winter of possible devastating Russian air strikes. Blackouts still remain common in parts of the country.

UK/ Geothermal energy

The country’s first deep geothermal energy project in nearly four decades began operations. Reaching almost 5 km below the surface, the well at the Eden Project in Cornwall will tap into waters with 200°C temperatures.

UK/ Nuclear power

Approval of the planned Sizewell C nuclear plant is lawful, London’s High Court ruled, dismissing a legal challenge. The NPP is owned by French energy giant EDF and has a capacity of about 3.2 GW.

U.S./ Solar power

A new venture by solar panel maker Vikram Solar (India) will invest up to $1.5 billion in the U.S. solar energy supply chain, starting next year with a factory in Colorado.

U.S./ Power grid

The Federal Energy Regulatory Commission and the North American Electric Reliability Corp warn that power plants remain vulnerable to cold weather. About 7 GW was unable to run in cold weather in late December across the Midwest and Eastern regions, leading to rolling power outages of more than 5 GW in the Southeast.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

ASEAN-Japan summit to mark 50 years of cooperation

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.